Nvidia Corp., the world’s most valuable company by market capitalization, has made a lackluster forecast for its revenue this quarter, suggesting that growth is slowing after two years of astonishing boom in artificial intelligence spending.

The company said in a statement on Wednesday that sales for the third fiscal quarter ending in October are expected to reach approximately $54 billion. Although this is in line with the average expectation on Wall Street, some analysts had previously predicted sales would exceed $60 billion.

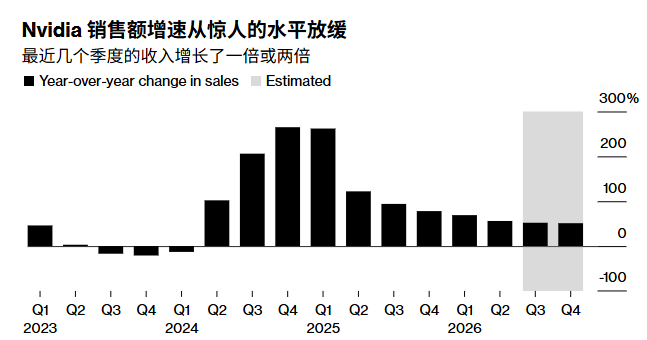

This prospect has intensified concerns that the pace of investment in artificial intelligence systems is unsustainable. The difficulties in the Chinese market have also cast a shadow over Nvidia’s business. Although the Trump administration recently relaxed restrictions on the export of some artificial intelligence chips, this relaxation has not yet translated into a rebound in revenue.

After the announcement, Nvidia’s share price dropped by about 3% in after-hours trading. As of the close of trading, Nvidia’s share price has risen by 35% this year, with its market value exceeding $400 billion.

During a Wednesday conference call with analysts, the company’s leadership denied that interest in deploying artificial intelligence infrastructure was waning.

“The future opportunities are huge,” said CEO Huang Renxun. “We expect that by 2020, the expenditure on artificial intelligence infrastructure will reach 3 to 4 trillion US dollars.”

The company also approved an additional $60 billion share repurchase program. As of the end of the second quarter, there was $14.7 billion remaining in Nvidia’s previous repurchase program.

Sales for the quarter ending July 27 rose 56% to $46.7 billion. That compared with the average market expectation of $46.2 billion. Although quarterly revenue increased by more than $16 billion from a year earlier, it was the smallest percentage increase in more than two years.

After deducting certain items, earnings per share for the second quarter were $1.05. Wall Street had expected earnings per share of $1.01.

The sales of the data center division were $41.1 billion, making it currently larger than any other chipmaker. In contrast, the average expectation was $41.3 billion. Gaming-related revenue (once Nvidia’s main source of income) was $4.29 billion. The average analyst expectation was $3.8 billion. The automotive division’s sales were $586 million, slightly below expectations.

Jacob Bourne, an analyst at Emarketer, said in a report that the research results show that if the short-term returns of artificial intelligence applications remain difficult to quantify, the spending of large data center operators “may tighten”.

Nvidia is still grappling with the impact of the intensifying competition between China and the United States. Semiconductor technology has become a major focus of contention between the two countries. In April this year, the Trump administration tightened restrictions on the export of data center processors to Chinese customers, effectively excluding Nvidia from the market. Washington later lifted the restrictions, stating that the United States would allow some Nvidia exports to China but would take a 15% revenue share.

Meanwhile, Beijing encourages the avoidance of US technology in AI systems accessible to the Chinese government. The changing policies make it difficult for Wall Street to predict how much revenue Nvidia can recover in the Chinese market. Some analysts predict its revenue will reach billions of dollars, while others refuse to predict any sales in China for the company until its situation becomes clearer.