Deutsche Bank said that the Federal Reserve’s withdrawal of liquidity support poses the greatest risk to the status of the US dollar as a reserve currency since the end of World War II.

Reuters this week, citing unnamed sources, said that the European Central Bank and regulatory officials held informal discussions about the possibility that the Trump administration might urge the Federal Reserve to withdraw from global funding markets during periods of market stress.

There are no signs that the Trump administration wants the Fed to reduce the so-called swap lines that the central bank provided during past crises. But the reported European discussions come at a time when the US is moving away from its European allies in other respects. George Saravelos, head of foreign exchange research at Deutsche Bank, wrote in a note to clients on Thursday that even if the Fed does not act, any concerns about the reliability of the swap lines could hurt the dollar.

Saravelos wrote: “If such concerns take hold among the US’s Western allies, it could generate the most significant global push to de-dollarize since the post-war global financial architecture was established.”

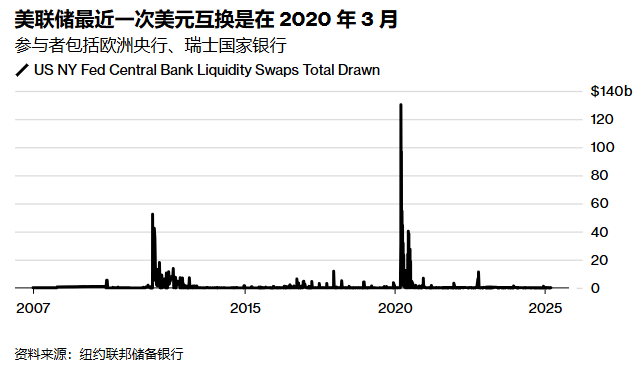

Currency swap lines were first introduced in the 1960s, allowing global institutions to borrow US dollars in exchange for their own currencies, thereby easing the demand for the dollar during periods of financial stress. As the financial crisis intensified, the Federal Reserve’s support through these lines was restored in 2007 and has long been regarded as an important backstop during times of market turmoil (though rarely utilized).

At present, the European Central Bank, the Bank of Japan, the Bank of Canada, the Bank of England and the Swiss National Bank have standing swap arrangements with the Federal Reserve. During the most severe period of market turmoil caused by the pandemic in early 2020, these swap lines were also extended to other central banks, including the Bank of Korea, the Central Bank of Brazil and the Bank of Mexico.

Saravelos pointed out that the Federal Reserve is fully responsible for its plans. But he said that the Trump administration could exert indirect influence on the central bank – either through “moral persuasion” or through the council members appointed by Trump.

Saravelos added that if the Federal Reserve were to choose to stop providing liquidity support under current pressure or attempt to use this tool as an exchange condition for achieving other policy goals of the United States, it would have far-reaching implications. As global institutions scramble to obtain US dollar funds, the US dollar would appreciate significantly, thereby driving up demand. This could also lead to the “dumping” of US assets that are often hedged in the foreign exchange swap market.

Most importantly, doubts about the Fed’s outstanding role as the world’s lender of last resort will “accelerate efforts by other countries to reduce their reliance on the US financial system,” Saravelos wrote. He pointed out that China and Russia are two major economies that do not have swap lines with the Fed and have accumulated non-US foreign exchange reserves and de-dollarized their economies in recent decades.

The Federal Reserve also offers other facilities aimed at easing global market liquidity problems. In March 2020, the Federal Reserve established repo agreement operations with a broader range of foreign institutions, which became a permanent operation in July 2021. This facility allows foreign institutions to exchange the US Treasury bonds they hold at the Federal Reserve for US dollars, rather than forcing them to liquidate US Treasury bonds or use the private repo market during periods of stress.