Traders are making big bets on a specific option that hinges on the dovish Federal Reserve cutting interest rates by more than a quarter of a percentage point next month.

Federal Reserve Chair Jerome Powell will deliver an important speech in Jackson Hole, Wyoming. These remarks may confirm or deny investors’ expectations for monetary easing policies. Meanwhile, inflation data has exceeded expectations, causing some traders to lower their expectations for interest rate cuts.

Despite a brief pullback, traders so far seem to remain convinced that interest rates will be cut next month, and U.S. Treasuries ended a three-day sell-off, sending yields on all maturities lower on Tuesday.

Ian Lyngen, head of US rates strategy at BMO Capital Markets, said in a note: “As the market prepares for Powell’s Jackson Hole speech, we believe the biggest risk for US Treasuries is that the Fed chair chooses to pour cold water on the widely expected September rate cut.”

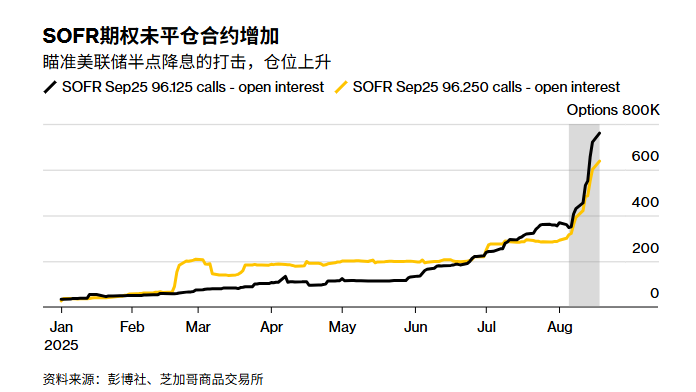

Since the beginning of this month, demand for the Secured Overnight Financing Rate (SOFR), which is closely related to policy expectations, has remained strong. This week, as the outstanding contracts targeting a half-basis-point rate cut soared, traders have once again ramped up their bets on SOFR.

Bloomberg analysis shows that if investors expect the Federal Reserve to cut interest rates by half a percentage point at its September policy meeting, then the current approximately 325,000 options (worth about 10 million US dollars) positions will make a profit of up to 100 million US dollars.

Even though the producer price index (PPI) for July, which was released last week, recorded the biggest increase in three years, indicating that tariffs are raising business costs, the growth in option positions has not abated. However, the data halted the rally in the bond market, pushed up short-term Treasury yields, and led traders to lower their expectations for rate cuts by the Federal Reserve at its remaining three policy meetings this year. Traders now expect a 25 basis point cut at the Fed’s September 16-17 meeting with about 80% probability.

Lin Gen said, “It is worth acknowledging that if Powell does not reach the dovish extent currently expected by the market, the front end of the curve could easily be subject to a bearish correction.”

Meanwhile, in the cash market, the latest survey of US Treasury clients by JPMorgan shows that investors have shifted from short positions to neutral positions, with the proportion of neutral positions currently at the highest level in about a month.

JPMorgan’s financial client survey shows that as of the week ending August 18, the direct short position of JPMorgan’s treasury bond clients dropped by 4 percentage points, turning to a neutral position. Currently, the proportion of direct short positions and neutral positions are at their lowest and highest levels since July 14, respectively.

Over the past week, there has been a significant increase in demand for SOFR options with strike prices of 96.125 and 96.25 on September 25, December 25, and March 26, which is reflected in the popular call option spread positions, indicating new risks. Meanwhile, a large amount of liquidation occurred for the option with a strike price of 95.625. The open interest of the December 25 put option and the March 26 put option decreased significantly.

Over the past week, the option skew at the long end of the Treasury yield curve has shifted in favor of put options, indicating that traders are paying a higher premium to hedge against the risk of selling long-term bond futures. However, the option skew from the short to medium term is slightly in favor of call option premiums, suggesting that traders are paying a higher premium to hedge against the risk of an increase in this part of the curve. The option skew indicates the demand for steeper positions through the options market.

CFTC data shows that as of the week ending August 12, asset management companies increased their net long positions in most bond futures varieties. Among them, the net long positions in long-term and ultra-long-term bond futures increased significantly. Hedge funds, on the other hand, increased their net short positions in 10-year US Treasury bond futures while covering their short positions in long-term bond contracts.