Banks such as Deutsche Bank and Wells Fargo have announced that the war-driven safe-haven rally of the US dollar may have come to an end as the fragile ceasefire agreement between the United States and Iran has prompted investors to seek riskier assets.

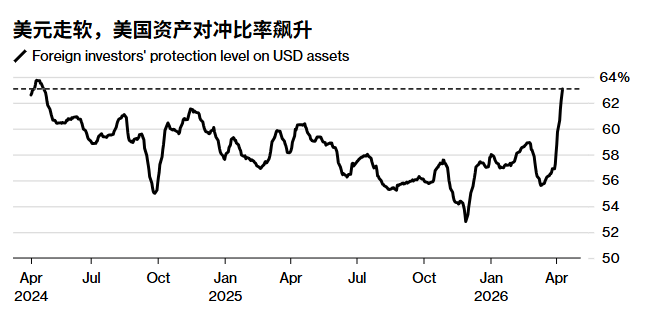

Banks believe it is time to short the US dollar, and global investors seem to be doing so. According to data from State Street Corp., the proportion of dollar hedging has risen to the highest level in two years. Meanwhile, confidence in the dollar in the options market has weakened, with positions being the most bearish on the dollar in weeks.

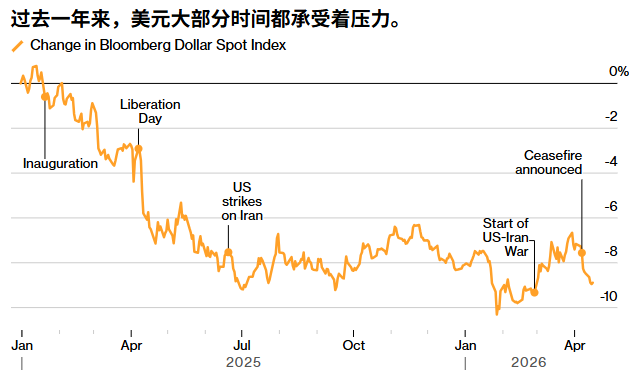

In March, as the war disrupted global markets, the Bloomberg Dollar Spot Index rose sharply, drawing investors to the world’s major reserve currency, the US dollar, which has long been regarded as a safe haven in times of crisis. However, over the past week, the dollar has given back most of its gains and is almost back to the level it was at before the war broke out at the end of February.

As a result, with the safe-haven aura fading, investors have once again focused on the negative factors that led to the dollar’s 8% decline last year – its worst performance since 2017 – including the prospect of interest rate cuts by the Federal Reserve.

“Funds have clearly rotated from safe-haven assets such as the US dollar to risk assets,” wrote Catherine Brooks, research director at London-based broker XTB, in an email. “If the US-Iran conflict can be resolved quickly, I think the US dollar will remain weak for some time to come.”

Since the US and Iran reached a ceasefire agreement on April 7, the Bloomberg Dollar Index has dropped by about 1.4%. During this period, risk-sensitive currencies led by those of Scandinavia, New Zealand and Australia have risen by about 3% against the US dollar, while the S&P 500 index has rebounded this week and hit a new high.

Pakistan is trying to mediate an extension of the ceasefire agreement beyond its official expiration date next week, but the situation remains tense. The fragility of the ceasefire agreement highlights the risk of being too bearish on the US dollar too early, especially if the breakdown of negotiations could trigger another round of oil price hikes and dash market expectations of the Fed’s easing policy.

The backdrop of persistently high crude oil prices highlights another reason for the dollar’s strength in recent weeks – the widespread belief that the United States, as an oil exporter, can be immune from energy shocks.

Citigroup’s currency analysts said on Thursday that from a risk-reward perspective, it is more favorable to bet on a stronger US dollar. They pointed out that persistently high commodity prices will limit the gains of risky assets, thereby supporting bond yields and the US dollar.

However, the relative easing of tensions has reignited concerns about the US dollar, which have been influencing discussions around the currency since Donald Trump became president last year.

Wells Fargo strategists recommend buying the Swedish krona against the US dollar. Deutsche Bank, on the other hand, suggests selling the broad dollar index, believing that the euro could eventually break through $1.20 from its current level of around $1.18, which would be the first time since January. JPMorgan strategists said last week that “in the medium to long term, the dollar seems to be on the decline due to this conflict,” partly because of the huge war expenses.

Some on Wall Street also believe that Trump wants to see a weaker dollar to support US exports, despite the current administration’s repeated reaffirmation of the long-standing “strong dollar” policy of the United States.

Against the backdrop of a shift in market sentiment, according to Morgan Stanley’s model, asset management companies increased their short positions on the US dollar in the first two weeks of April. A survey by Bank of America from April 3 to 9 (overlapping with the effective date of the ceasefire agreement) showed that the most favored trading strategy by fund managers this year (second only to holding bonds) was shorting the US dollar.

“Investors view the impact of a potential war with Iran on the dollar’s trajectory in 2026 as more of a horizontal shift rather than a change in trend,” wrote Bank of America strategists Ralf Preusser and Meghan Swiber in a report this week.

International investors shorting the US dollar through derivatives to eliminate currency risks in their US assets is another potential trigger for the dollar’s weakness.

Data from State Street, one of the world’s largest custodian banks, shows that they are increasing their hedging efforts. After the ceasefire statement was issued, the hedging ratio for the US dollar has risen to 63%.

Moreover, the resolution of the war, by reducing concerns about economies outside the United States, might stimulate investors to purchase more international assets.