Bond traders are ramping up their bets that the next policy move by the Federal Reserve could be a rate hike rather than a cut.

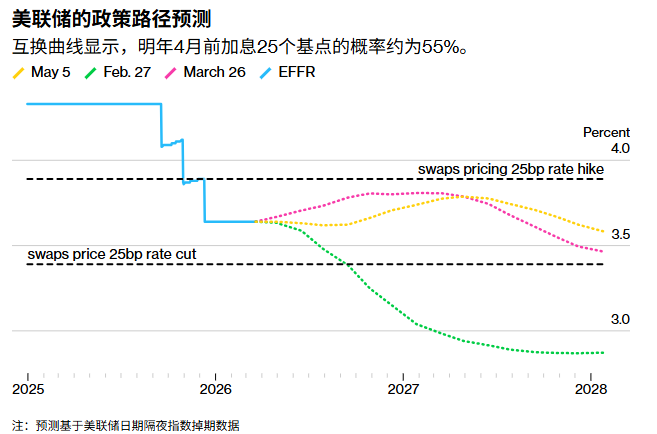

Swap contracts linked to the central bank’s interest rate decisions currently indicate that the probability of the Federal Reserve raising interest rates before April next year exceeds 50%, and it will not ease monetary policy until then. More and more traders are also increasing their positions to hedge against the rising probability of an interest rate hike before the end of the year.

This shift in the market comes at a time when policymakers seem increasingly divided over the outlook for interest rates, and just as Kevin Warsh is set to take over as chair of the Federal Reserve following US President Donald Trump’s push for lower rates.

Lawrence Gillum, chief fixed income strategist at LPL Financial, believes that although there is still a possibility of interest rate cuts this year, the longer the conflict with Iran persists, the less likely a rate cut will be. “There is no doubt that Powell will face a difficult situation in the future,” he said.

Futures and options trading closely related to the Secured Overnight Financing Rate (SOFR) intensified ahead of Friday’s U.S. jobs report. The rate is closely tied to policy expectations. The employment data may indicate that the labor market situation is stabilizing, thus making inflation risks a focus of investors’ attention.

A stable labor market will enable the Federal Reserve to focus on addressing the inflationary shock from oil until that situation persists, and then consider rate cuts, wrote Marco Casiraghi, senior economist at Evercore ISI, and analyst Gang Lyu in a report, adding that their base view is that the war may delay rate cuts but will not prevent them.

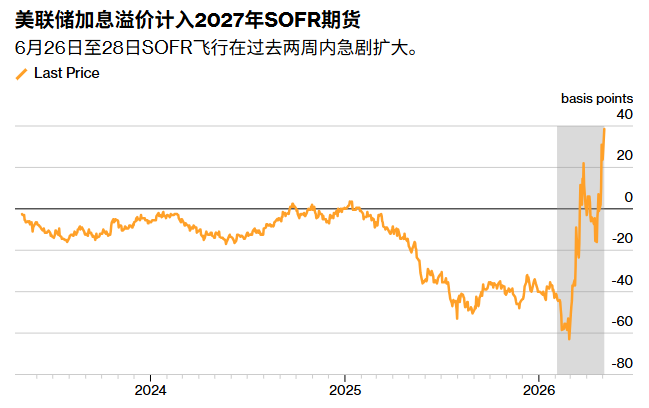

In the swap market, the possibility of a rate cut has been pushed back to early 2028, with the Fed swap rate for March 2028 trading 8 basis points below the current effective Fed funds rate.

The weakness in the SOFR futures market is mainly reflected in the June 2027 contracts. Over the past few weeks, these contracts have performed far worse than market expectations, as traders have yet to factor in the possibility of interest rate hikes a year from now into the prices. This has led to a significant expansion of the 2026-2027-2028 June delivery butterfly option spread to a cyclical high.

“The front end of the US interest rate curve has yet to respond meaningfully to the possibility of a rate-hiking cycle in the next six to twelve months,” said Bridger Kurrana, portfolio manager at Wellington Management, adding, “It’s surprising that the US is still reluctant to accept the idea of a possible rate-hiking cycle.”

In the SOFR options market, on Monday and Tuesday, there was a large amount of buying of funds that hedge against the possibility of an increase in interest rate premiums within a year.

Chicago Mercantile Exchange futures market data released on Tuesday showed that both positions were closed and opened simultaneously, indicating that traders were pushing their short positions further into 2027, when the expectation of interest rate hikes has peaked.

Guillaume of LPL stated, “We still believe that the threshold for raising interest rates is much higher than that for maintaining stable rates.”

Over the past week, the spot market also witnessed a bearish trend. A survey of JPMorgan Chase clients revealed that investors were increasing their short positions and adopting a neutral stance. The rise in short positions came as the 30-year US Treasury yield hovered around 5% after falling below a key level for the first time this year.