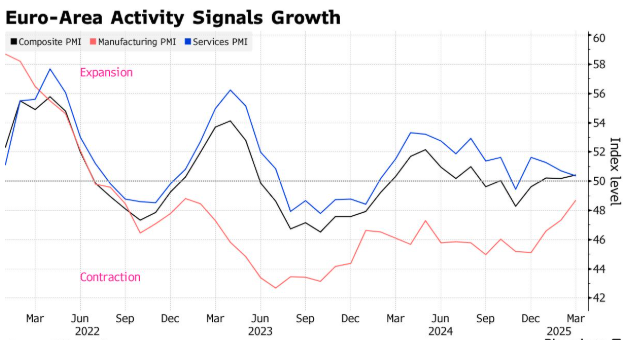

Business activity in the eurozone reached its highest level in seven months as manufacturing rebounded more strongly than expected and spending in Germany rose sharply.

The S&P Global Composite Purchasing Managers’ Index rose slightly to 50.4, further above the 50-point expansion and contraction dividing line. Analysts had previously expected the index to be slightly above 50.7.

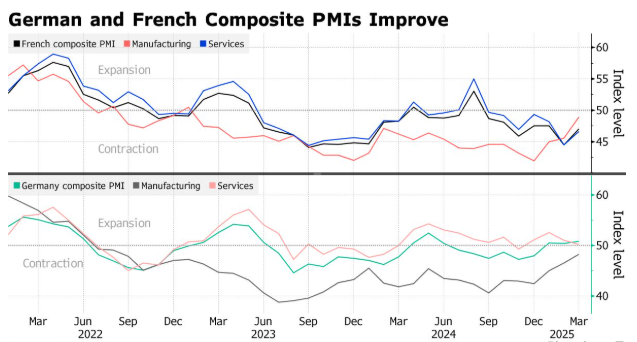

This growth is mainly attributed to Germany, where a plan to spend hundreds of billions of euros on infrastructure and defense will help the continent’s largest economy shake off five years of economic stagnation.

However, the situation in France has also improved, although its index remains below 50, it still exceeded analysts’ expectations as factories have resumed some operations.

Cyrus de la Rubia, an economist at Commerzbank in Hamburg, said in a statement on Monday: “Given that Europe is willing to invest heavily in defense and infrastructure and that Germany just approved a historic fiscal package last week, there seems to be good reason for more sustained hopes of recovery.”

The region’s sluggish economy is not only expected to get a boost from Germany’s financial support, but also from the continent-wide rearmament drive in response to the reduction of US military support. Factories, which have long been a weak link (especially in Germany), will be the biggest beneficiaries, even if such improvements take several months to materialize.

Although manufacturing performed better than analysts’ expectations, the service sector, while still growing, remained below expectations.

The Bloomberg Dollar Spot Index has dropped nearly 4% since its January closing high, offering some relief to U.S. companies that operate overseas and expect to suffer a significant foreign-exchange shock in the coming year.

Howard Du, a foreign exchange strategist at Bank of America, said that a depreciation of the US dollar could “directly boost and enhance corporate profits,” adding that the impact of a dollar depreciation on corporate earnings could be greater compared to that of a dollar appreciation. Du noted that, on average, about 30% of the revenue of S&P 500 companies comes from outside the United States.

Citigroup analysts noted in a report that the recent trend could imply that the currency headwind for fiscal 2025 will be smaller than McCormick & Co Inc.’s initial expectations. Brian Andrews, the chief financial officer, said in Cooper Cos Inc.’s medical device earnings call in early March that a weaker dollar could also put the company “in a good position” to reach or exceed the upper limit of its earnings per share forecast. About half of Cooper’s revenue comes from outside the United States.

After the dollar’s surge in the fourth quarter of last year hit the profit prospects of some of the world’s largest companies, including Amazon and Apple, the earnings of these companies have improved. Driven by strong US interest rates and the election of President Trump, the Bloomberg Dollar Index rose by more than 7% from October to December.

This year, the trend seems set to continue, prompting warnings from companies such as McDonald’s, which expects its 2025 profits to be affected by 20 to 30 cents per share, and Uber Technologies Inc., which anticipates a greater foreign exchange impact in the first quarter.

The US dollar dropped by 2.3% in the first week of March, and market sentiment shifted rapidly. As European countries increased their defense spending, the euro rose against the US dollar, while the uncertainty caused by tariff issues soared.

Technical analysis:

Gold: Yesterday, we clearly pointed out in the article that “for today, we continue to pay attention to whether the price will retest around 3005 and attempt to buy at the new demand zone.” The price actually dropped to 3002 overnight and then rebounded, but it is currently temporarily blocked at the 3010/15 area. For today, we need to start paying attention to the momentum breakthrough performance at 3010/15. For detailed positions, please consult the plugin.

(Gold 15-minute chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the chart, please contact V: Hana-fgfg.

Nasdaq: Yesterday, we clearly reminded in the plugin of the buy stop momentum break trading after the blue area was broken through. The price, after breaking through 20,142, continued to strengthen to around 20,400. Our buy stop operation yesterday gained over 260 basis points. Today, we hope the price can slightly pull back, seek a new demand area, and then test for an upward movement. For detailed positions, please consult the plugin.

(NASDAQ 15-minute chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the chart, please contact V: Hana-fgfg.

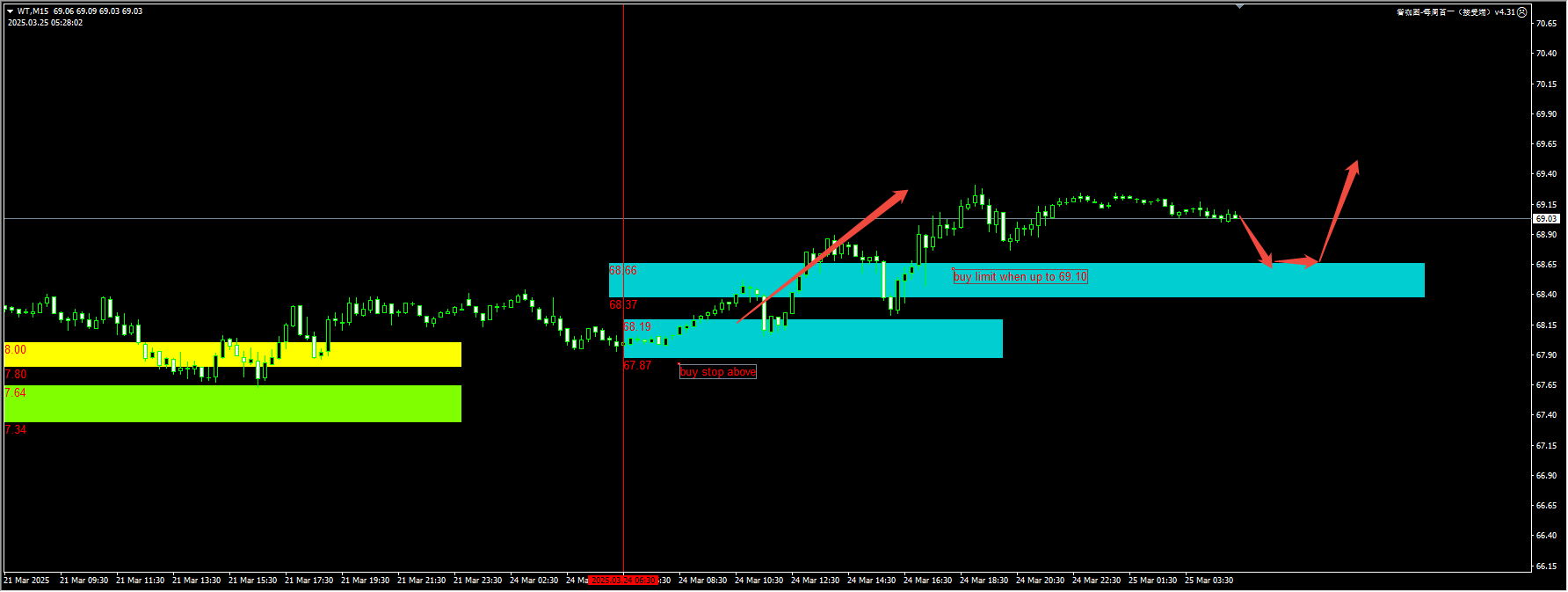

Crude oil: Yesterday, we clearly reminded twice in the plugin about the trading of momentum breakouts. The first one was a buy stop operation at 68.19, which could have reaped over 100 basis points in gains; the second opportunity to retrace to 68.66 did not materialize, but this area remains a key retracement confirmation signal to watch out for intraday. For detailed positions, please consult the plugin.

(Crude Oil 15-Minute Chart)

(Crude Oil 15-Minute Chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the picture, please contact V:Hana-fgfg.

Today’s key financial data and events to focus on:

17:00 Germany March IFO Business Climate Index

19:00 UK CBI Retail Sales Forecast Index for March

At 21:05, William, the president of the Federal Reserve Bank of New York, delivered the opening remarks at an event.

22:00 US Conference Board Consumer Confidence Index for March