Recently, Musk has been making big moves in the “government efficiency department”, but the share price of his original “main business” – Tesla – is experiencing some troubles.

Tesla’s (TSLA) share price dropped by 5.7% in Tuesday afternoon trading, falling to its lowest level since about 10 days after the US election. Earlier in the day, BYD Company announced that it would offer new advanced driver-assistance features for free on most of its product lines, shocking the electric vehicle industry.

Analyst Colin Rusch and his team believe that Elon Musk’s bid for OpenAI is merely a temporary distraction from other challenges. Rusch pointed out that the bid price for OpenAI is 38% lower than the company’s financing level in October last year.

We do not expect any meaningful discussions. However, as competition in the electric vehicle and self-driving car sectors intensifies, we believe that Wall Street’s valuation of TSLA is facing increasing risks. We also think that while CEO Musk’s political activities have fans in certain circles, as the Trump administration tests the limits of its power, his public life may alienate consumers and employees.

Tesla derives 90% of its revenue from car sales, leasing, services and related income. This includes used car sales, public charging and warranty sales. Therefore, despite management’s efforts to rebrand the company as an AI firm, car sales remain crucial to Tesla’s bottom line and valuation.

However, selling Tesla vehicles has always been challenging. Tesla’s sales growth rate dropped to 40% in 2022, then to 38% in 2023, and for the first time fell to -1% in 2024.

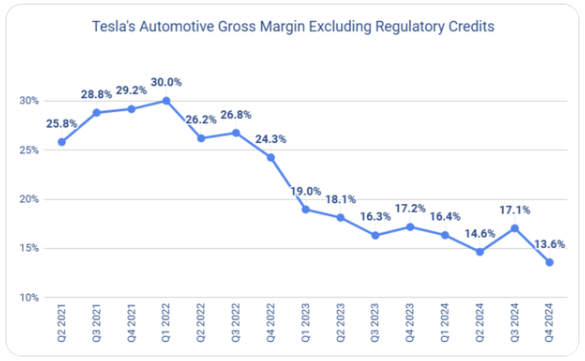

As shown in the following figure, Tesla not only has seen its growth stall but also its profit margin decline. Please note that these figures do not include regulatory credits, but do include the increase in Tesla’s profit margin due to the $7,500 electric vehicle tax credit, which enabled Tesla to charge higher prices than it would have without the tax credit.

Without this year’s $7,500 new electric vehicle tax credit and $4,000 used electric vehicle tax credit that are at risk of being cancelled, as well as the $1.4 billion manufacturing credit that reduced Tesla’s cost of revenue (2024 10-K p:58), Tesla’s profitability would have been even lower.

Tesla’s first-quarter deliveries are expected to be 376,000 vehicles, the worst in three years. Although Tesla made a profit in 2022, the last time its quarterly deliveries were this low, the company’s expenses have increased significantly since then. As shown in the following chart

Due to the high interest rates in the United States and the intense competitive pressure from automakers in China and other parts of the world, Tesla’s car sales will continue to face challenges in the first quarter of 2025 and for the remainder of this year.

Furthermore, if Tesla delivers fewer than 400,000 vehicles in the first quarter, I expect it will fail to meet the consensus estimate of $0.52 per share, due to low factory capacity utilization resulting in a higher allocation of fixed costs because of a lower number of units sold.

In China, Tesla Energy may face competition that is as fierce or even more intense than that of Tesla vehicles. The reason is simple: Tesla’s stationary energy storage products are mainly composed of battery cells, while battery cells account for only a small portion of the total parts and value of Tesla vehicles. Due to this simple reason, Chinese competitors may replicate Tesla or even surpass it at a speed even faster than that at which BYD overtook Tesla.