The Bureau of Labor Statistics of the United States will release the labor market report for February on March 7th. The market generally expects that the non-farm payrolls will increase by 153,000, higher than the 143,000 in January, and the unemployment rate will remain unchanged at 4%, or still close to full employment.

If the actual data meets expectations, it indicates a tight labor market, consistent with a moderately strong economy. The problem is that the US economy had already fallen into recession in the first quarter of 2025 and is deteriorating rapidly.

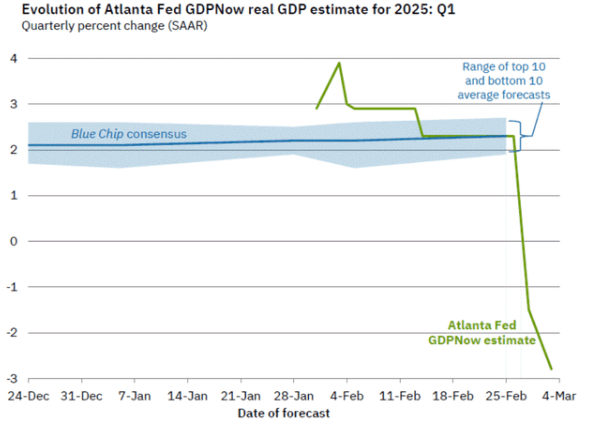

Specifically, the Atlanta Fed’s GDPNow currently indicates that the GDP for the first quarter of 2025 is expected to decline by -2.8% – this would be one of the largest contractions ever, aside from the COVID-19 pandemic in 2020 and the financial crisis in 2008.

The main reason for the expected 2.8% contraction in the first quarter is the trade deficit; as companies rushed to import industrial supplies and capital goods before tariffs took effect. However, PCE consumer spending also seems to be declining, currently contributing only 0.1% to overall GDP. For comparison, on February 26th, it was estimated that consumer spending contributed 1.56% to GDP, while a week earlier it was estimated at 2.3%.

Therefore, the February labor market report is likely to confirm this weakening trend, and the actual data may unexpectedly decline. The main reasons for the expected weakness in the February labor market include Trump’s restrictive immigration policies and the DOGE government’s spending cuts.

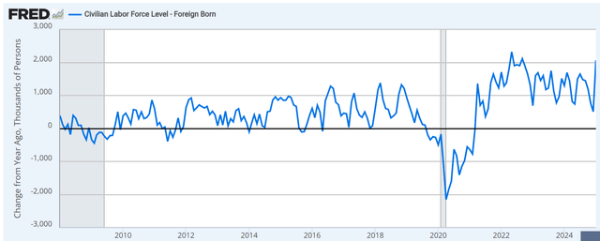

The first issue worth noting is how Trump’s restrictive immigration policies will affect the labor force, especially the foreign-born labor force.

The Trump administration reversed Biden’s policies, conducting large-scale deportations from day one and strictly controlling the border to prevent illegal crossings.

Therefore, it is expected that the foreign-born labor force will decline, which will be reflected in a drop in the unemployment rate (if the reduction in the labor force exceeds the increase in the number of unemployed) – this will mean that labor shortages will reappear, and wage increases will bring new inflationary pressures. At the same time, the slowdown in consumption related to immigration may have an impact on our economy and lead to unemployment in other sectors.

Another key policy of the Biden administration is to increase government spending and create more government jobs, which accounted for about 25% of all new jobs added last year.

The Trump administration also reversed this policy through DOGE, freezing federal government hiring and beginning to lay off many federal government employees. This could also be reflected in the form of government job losses in the February labor market report.

Please note that most government jobs are in local governments. However, the DOGE austerity measures taken by freezing grants and reducing overall federal government spending may also lead to job losses in local and state governments.

The number of foreign workers in the US increased by 2 million in the past 12 months, but it is currently projected to be negative.

The ISM’s manufacturing survey for February indicates that manufacturing jobs are on the decline, with the employment index dropping below 50 to 47. As a result, it is highly likely that manufacturing jobs also decreased in February.

The S&P Global Index report for February indicated that “the service sector, after two consecutive months of net hiring, has once again seen layoffs.” Therefore, this might also be reflected in the layoff situations across different service sectors.

GDPNow indicates that recent economic data suggest the U.S. economy is sliding into a recession. The Russell 2000 (IWM), a proxy for economically sensitive small-cap stocks, has fallen by more than 5% so far this year – and the Russell 2000 was a soft landing trade.

However, the current weak data is limited to survey data regarded as leading indicators. This weakness must eventually be confirmed by the government’s official labor market data.

Whether the February labor market report confirms that a recession is underway remains to be seen. The reference period for the report was February 12, before the recent negative data was released.

In addition to the decline of stock markets such as the Nasdaq 100 Index (QQQ) and the S&P 500 Index (SP500), which have a relatively high proportion of technology stocks, the bond market also performed strongly, with the 10-year bond yield (US10Y) dropping to 4.16%, which also supports the unfolding of the economic recession theory.

However, the main problem is that the survey results also show that inflation expectations have risen, mainly due to tariffs. Therefore, despite the significant economic slowdown, the Federal Reserve may not be able to cut interest rates significantly, which could lead to further declines in the stock market. This is the danger of stagflation.