Consumer inflation slowed in February, which may give the Federal Reserve more leeway to keep the target interest rate unchanged when it announces a revised policy stance this week (Wednesday, March 19). However, against the backdrop of rapidly escalating tariffs, last month’s data is already in the past, so the uncertainty about how the Fed will manage policy in the coming weeks and months has increased.

For monetary policy, this challenge is particularly complex, as the threat of rising inflation may at least in the short term be accompanied by a slowdown in economic growth due to the increase in tariffs.

The Federal Reserve remains highly vigilant about new inflationary pressures, but the data available so far is not particularly useful for assessing the inflation risks related to tariffs, as it takes weeks or even months for clear signals to emerge in the economy.

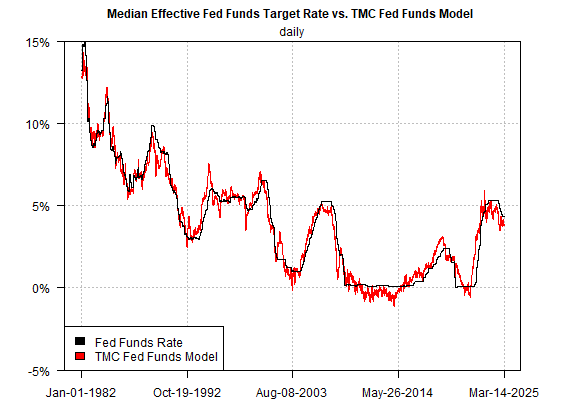

Today’s federal funds futures prices almost certainly indicate that the Federal Reserve will keep the target rate unchanged at 4.25% to 4.50% on Wednesday. Market expectations for the Fed to hold rates steady at the next FOMC meeting on May 7 have dropped to around 76%, but this forecast should be taken with caution as it largely depends on the data to be released in the coming weeks (as well as how or if the tariff policy changes).

The president reaffirmed today that the United States will still begin to widely implement reciprocal tariffs and industry tariffs on April 2.

Although the short-term interest rate outlook is stable, the Federal Reserve may face a dilemma, as at least in theory, two competing forces could push policy adjustments in opposite directions. As mentioned earlier, due to the escalating tariffs, the risk of inflation rising may be lurking in the short term. If inflation does pick up, this shift would imply that tightening monetary policy would be appropriate.

The same tariffs could also slow economic growth, making it necessary to cut interest rates. Although there is no convincing hard data to clearly indicate a substantial slowdown in US economic growth at present, an increasing number of forecasts and predictions suggest that there may be a certain degree of slowdown in economic growth, mainly based on the view that tariffs will continue to be imposed and may even expand as other countries respond. The recent sharp increase in the search volume for the word “recession” on Google indicates that the unease about the economic outlook is beginning to resonate in the public domain.

Investors will be closely watching the Federal Reserve’s press conference on Wednesday to see how Fed Chair Jerome Powell and the Federal Reserve Board consider assessing inflation and economic activity risks related to the labor market. The Fed will also release new economic forecasts, which will provide a reference for the central bank’s revised expectations.

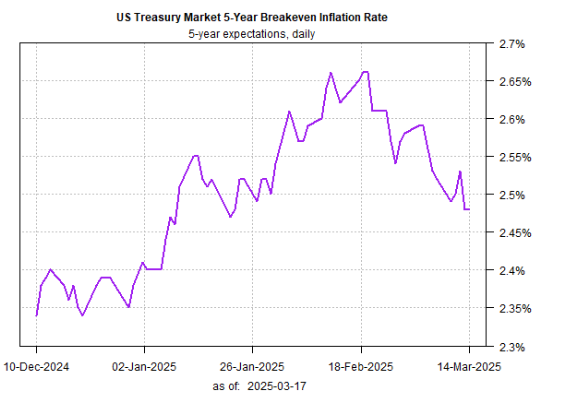

An encouraging real-time signal on inflation is that the US Treasury market has been continuously lowering inflation expectations, which are based on the 5-year breakeven rate, that is, the spread between the nominal 5-year yield and the inflation-indexed yield. As of Friday (March 14), the spread was stable at 2.48%, having peaked at 2.66% in mid-February.

Encouraging, but concerns over economic activity could lower inflation expectations. In this case, if the weak economic factors prevail, the Federal Reserve may soon be forced to cut interest rates.

At present, policymakers are generally adopting a wait-and-see attitude. In the foreseeable future, managing market expectations regarding how and in what direction the central bank’s policies will adjust will be the top concern. Powell may face the biggest policy challenge of his tenure – and this challenge will begin at Wednesday’s press conference.