Frightened by the prospect that Donald Trump’s trade war could trigger a global recession, investors have flocked to the US Treasury market – at least for now, they are ignoring the risk that the same punitive tariffs could spark another round of inflation.

After U.S. government bonds rose, pushing the two-year Treasury yield to its lowest level since 2022, traders are preparing for further gains and see a greater possibility that the Federal Reserve will take the most aggressive rate cuts to prevent an economic slowdown. While short-term bullish sentiment may be justified, Kathryn Kaminski of AlphaSimplex Group said that investors focused on economic growth slowdowns have ignored Federal Reserve Chair Jerome Powell’s comments on the impact of tariffs on inflation, and they will suffer the consequences.

Kaminski, chief strategist and portfolio manager at AlphaSimplex, said: “The market has reacted strongly to the possibility of a slowdown in economic growth and a disruption in demand. This should put the Federal Reserve in a difficult position. They may cut interest rates based on the economic slowdown, but inflation could complicate this process. The market seems increasingly inclined to view tariff news as very bad news. We believe that it is the right choice to go long on bonds now.”

Stagflation, which refers to economic slowdown and rising prices, will upend the bond market. In his speech on Friday, Powell acknowledged that tariffs might make policy implementation difficult.

He said: “Although tariffs are likely to cause inflation to rise at least temporarily, their impact could also be more lasting.” He reaffirmed that the central bank is in no hurry to adjust interest rates.

Despite this, the activity in futures contracts related to the Fed’s 2026 meetings has shifted from an expectation of less than three rate cuts to nearly four by December. Other futures trading conducted last week suggested that the Fed might act slowly, a result that would ultimately lead to a larger rate cut next year.

This stance indicates that Fed officials are in a difficult position as they are concerned about the short-term inflationary impact of the implementation of tariffs. Michael Gapen, chief U.S. economist at Morgan Stanley, has put forward this view and has pushed back the next rate cut from June to next year.

Priya Misra, a portfolio manager at JPMorgan Asset Management, said, “The longer the Fed waits to cut interest rates, the more it will need to cut in total.”

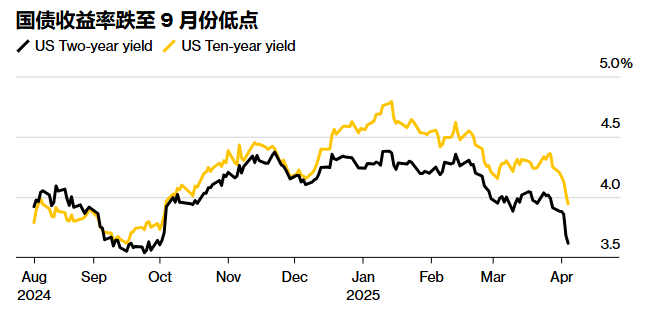

Since Wednesday, investors have clearly been seeking safety in the bond market as they bet that the US might fall into an economic recession. After Trump announced tariffs on US trading partners, yields on policy-sensitive US Treasuries dropped by more than 0.4% at one point.

This pushed the two-year Treasury yield close to 3.5% – the lowest level since September 2022. Meanwhile, the 10-year Treasury yield briefly fell below 4% for the first time since October. In the Asian session on Monday, the benchmark 10-year Treasury yield dropped as much as 11 basis points to 3.88%.

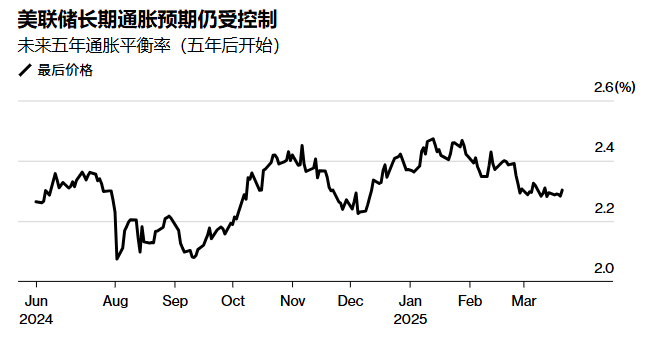

Daniel Ivascyn, chief investment officer of Pacific Investment Management Co., said: “We are in a period of extreme macro uncertainty. Given that inflation has risen and may continue to do so, the nature of this shock is different from those in the past few decades.”

The U.S. consumer price inflation data for March will be released on Thursday. It is expected that the annual figure will still be above the Federal Reserve’s 2% target, but the data does not take into account the impact of tariffs.

There is a debate in the market over whether foreign countries will reduce their purchase of US Treasury bonds as a form of retaliation. According to the latest data from the US government, China and Japan are the largest overseas holders of US sovereign debt. The former has been cutting its US Treasury bond reserves for three consecutive years, while Japan’s US Treasury bond reserves have also declined.