The “sell US Treasuries” trade that has swept through the market this month could deal a lasting blow to investors’ willingness to hold the longest-dated bonds of the US government, a mainstay of financing the US deficit.

For bond managers at BlackRock, Brandywine Global Investment Management and Vanguard, the problem is that as President Donald Trump approaches his 100th day in office, he has created more and more uncertainties, forcing traders to focus on a wide range of issues rather than just possible interest rate movements.

For instance, what do Trump’s trade war, tax cut agenda and aimless policy-making mean for an already sluggish economic growth, stubborn inflation and a huge fiscal gap? Will he threaten to fire Federal Reserve Chair Jerome Powell again? Is he actively seeking a depreciation of the US dollar?

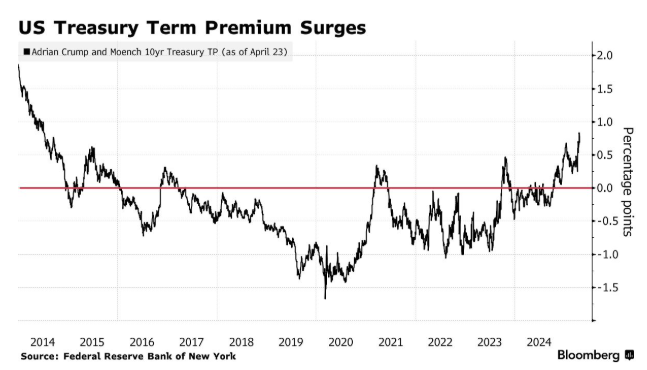

The result is that risk awareness has increased, prompting bond buyers to question the traditional safe-haven status of US Treasuries and demanding higher yields for longer-term bonds. To some extent, this additional buffer (which traders call the “term premium”) has reached its highest level since 2014.

“We are in a new world order,” said Jack McIntyre, whose team manages $63 billion of Brandivian’s assets. “Even if Trump makes concessions on tariffs, I think the level of uncertainty will still rise. That means the term premium will remain high.”

Of course, if Trump reaches a trade deal or continues to hint at his concerns about a full-scale collapse of the bond market, worries surrounding US Treasuries may ease. But as Treasury Secretary Scott Bessent prepares to unveil the government’s latest borrowing plan on Wednesday, he faces an additional task: soothing investors who are grappling with growing concerns.

All this uncertainty has led McIntyre to maintain a roughly neutral view on his benchmark interest rate. It has also changed his outlook on long-term bonds in a slowing economy. In short, he says yields will still be higher than he originally expected.

JPMorgan Asset Management believes that US Treasuries are more attractive than European government bonds. The auction of 30-year US Treasuries held this month indicates that there is still demand for maturing bonds in the market – and the prices are also reasonable. The auction results have alleviated concerns about buyers’ boycotts, and long-term bond yields have also fallen from recent highs.

However, market sentiment remains fragile. For instance, although Trump stated last week that he had “no intention” of firing Powell, his criticism of the Fed chair has made some investors worry about the independence of the Federal Reserve.

Pacific Investment Management Co. compared the triple weakness of the dollar, the U.S. stock market and U.S. Treasuries this month to a possible trend in emerging markets, and the company has also been buying U.S. Treasuries. But it has been limiting the fluctuation range of the yield curve. The bond management company, which manages $2 trillion in assets, currently favors bonds with maturities of 5 to 10 years.

There are other signs that investors are worried about the long-term bond market: the yield on 30-year Treasury bonds adjusted for inflation reached its highest level since the financial crisis this month. Although it has since fallen, it remains higher than it was on April 2 when Trump announced his plan to impose tariffs across the board.

For Vanguard Group, there is still room for further increase in the built-in additional insurance in long-term bonds, especially if the federal deficit expands and leads to an increase in bond issuance.

Rebecca Ventur, senior fixed income product manager at the asset management company that manages about $10 trillion in assets, said: “The term premium is no longer at a low level, but you can’t prove that it’s at a historical high. When you look at the backdrop of fiscal risks, the term premium may increase over time.”

Vanguard Group expects the U.S. economy to grow by less than 1% this year, which will be the lowest level since 2020. Venter said, “This is not a good sign for the U.S. budget deficit.”

BlackRock Investment Institute said in a report that the sell-off in the US market “indicates that people are seeking more risk compensation and has brought this fragile balance into focus.”

George Catrambone of DWS Americas believes that given the various changing signals from the White House on tariffs and other policies, the term premium may fall back, but the extent will also be limited.

“Once the situation becomes clearer and an agreement is reached, I expect the term premium to decline,” the company’s fixed income chief said. “But it won’t return to the lows of the past decade because fiscal problems will always be there.”

In the mid-1970s, when the US dollar replaced gold as the world’s reserve asset, central banks around the world rushed to purchase US Treasury bonds to hold their dollar reserves. As the federal government has never broken its promise to repay debts, US Treasury bonds have been regarded as a stable investment.

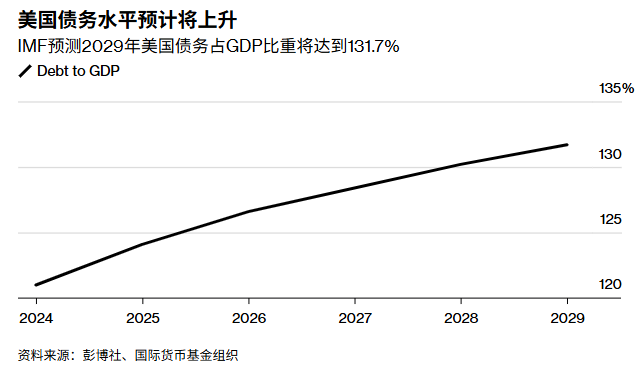

The US national debt currently stands at 121% of its gross domestic product (GDP). When Trump took office, he bet that he could reduce the budget deficit by stimulating economic growth through tax cuts. Recently, he has also hinted that tariff revenues will help ease the burden of the national debt.

But others are worried that his policies will only exacerbate the national debt. Trump is trying to make the tax cuts he implemented during his first term permanent, and he also plans to implement more tax cuts. If tariffs lead to a recession, the government may face pressure to increase spending.

Mike Riddell, a fixed income portfolio manager at Fidelity International, said that given this, the spiraling rise in US Treasury yields could signal a trend of “capital flight” as foreign investors become increasingly reluctant to finance the US deficit. “The global ‘bond vigilantes’ are clearly still active,” he said.

A major US trader: Tariffs on China may cause a supply shock to the US economy.

For nearly a month, President Donald Trump’s tariff offensive has swept through Washington and Wall Street. If the trade war continues, the next turmoil will hit the United States more directly.

Since the US raised tariffs on China to 145% in early April, the volume of goods transportation has plummeted, with estimates suggesting a drop of up to 60%. The significant reduction in goods from one of the US’s largest trading partners has not yet been felt by many Americans, but this situation is about to change.

By mid-May, tens of thousands of companies, large and small, will need to replenish their inventories. Walmart and Target told Trump at a meeting last week that consumers may see empty shelves and price hikes. Torsten Slok, chief economist at Apollo Global Management, recently warned that industries such as trucking, logistics and retail are about to experience shortages and large-scale layoffs similar to those during the pandemic.

Although Trump has shown a willingness to be flexible in recent days on the issue of imposing import taxes on China and other countries, it may be too late to prevent supply shocks from affecting the US economy, and these shocks could persist until Christmas.

“Time is tight,” said Jim Gerson, president of Gersons Companies. The 84-year-old firm supplies holiday decorations and candles to major U.S. retailers. Based in Olathe, Kansas, more than half of its products come from China, and currently about 250 containers are waiting to be shipped.

“We must solve this problem,” said Gerson, the third-generation leader of the family business, which has an annual sales volume of approximately 100 million US dollars. “Hopefully, it will be achieved soon.”

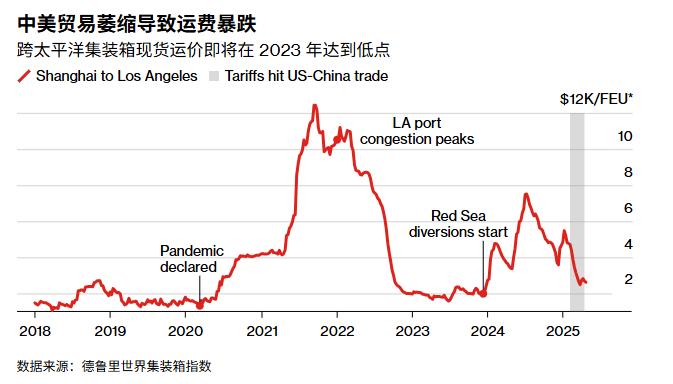

Even if hostilities ease, restarting trans-Pacific trade will bring additional risks. The shipping industry has cut capacity in response to weak demand. This means that a sudden surge in orders resulting from improved relations between the superpowers could overwhelm the entire shipping network, causing delays and pushing up costs. A similar situation occurred during the pandemic, when container prices tripled and an oversupply of cargo ships led to port congestion.

Lars Jensen, CEO of the shipping consultancy Vespucci Maritime, said: “The number of ports will surge, and so will the volume of truck and rail traffic, causing delays and bottlenecks. Ports are designed to ensure a stable flow, not to handle the fluctuations in transport volume.”

The United States’ imposition of tariffs on China comes at a crucial time for the retail industry. March and April are when suppliers start to increase inventory for the second half of the year to meet back-to-school and Christmas orders. For many companies, the first batch of holiday goods should arrive in the United States in about two weeks.

“We’re paralyzed,” said Jay Foreman, CEO of Basic Fun, a toy manufacturer in Boca Raton, Florida, which supplies products to large retailers such as Amazon.com Inc. and Walmart. He called the tariffs “de facto embargoes” and said that customers have so far been putting orders on hold, but he expects that if the tariffs on China remain at this level for much longer, customers will start canceling orders.

“Things started to really deteriorate a few weeks ago,” said Forman. His company has annual sales of about $200 million, with about 90% of its products coming from China. “We are currently in a period where losses are manageable, but the extent of the losses is increasing every week.”

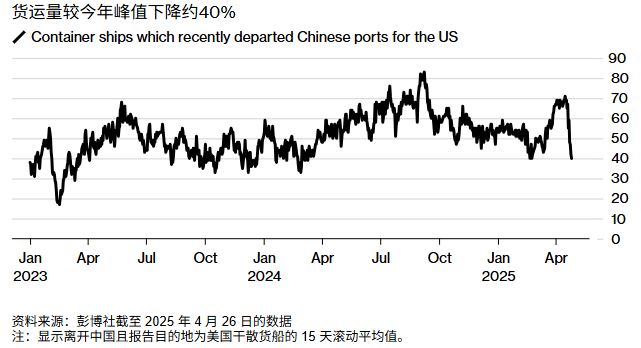

The front of this supply shock is particularly evident in Asia. According to ship-tracking data compiled by Bloomberg, about 40 cargo ships that recently docked at Chinese ports are currently sailing to the United States, a decrease of approximately 40% compared to early April.

Data shows that these ships carried about 320,000 containers, a reduction of approximately one third compared to the number after Trump announced that he would raise tariffs on almost all Chinese goods to 145%.

Judah Levine, the research director of the freight booking platform Freightos, said that many US importers will take advantage of the 90-day reprieve of what Trump called “reciprocal tariffs” to order goods in advance from other US trading partners. This may help ease any China-centered shock through ports and logistics networks.

Due to the high prices of Chinese goods, some shippers in the United States have begun to turn to suppliers in Southeast Asia.

Hapag-Lloyd AG, the world’s fifth-largest container shipping company, said in an email statement last week that about 30% of orders from China to the United States had been cancelled. However, the Hamburg-based company said that business from exporters in Cambodia, Thailand and Vietnam had grown significantly.

However, Levin said that the shock effects on the economy in the coming months may still be difficult to overcome. He said, “There is likely to be a significant slowdown. The restart may cause some congestion. The strength of the rebound and the resulting chaos may be related to the length of the pause.”

As China’s demand for US goods has rapidly declined, shipping companies have been cutting capacity to prevent a sharp drop in ocean freight rates. According to data cited by industry veteran John McCown, about 80 flights from China to the US were cancelled in April, which is about 60% more than any month during the COVID-19 pandemic.

In a recent research report, McCown stated: “It is fair to say that the container shipping industry has never faced such macro headwinds as it does now.”

The World Trade Organization has warned that trade in goods between the United States and China could fall by 80%, lending support to US Treasury Secretary Scott Bessent’s description of the current situation as essentially a trade embargo.

This uncertainty is part of the reason why economists say a US recession is almost a coin toss. Forecasters surveyed by Bloomberg expect imports to fall at an annualized rate of 7% in the second quarter, the biggest drop since the pandemic began.

The imminent supply shock has prompted economists to raise inflation forecasts as it could push up prices. Business executives say that the prices of some Chinese goods could double. And this is happening at a time when consumer confidence has sharply deteriorated.

If the trade war between the United States and China continues for a few more weeks, suppliers and retailers will have to make some tough decisions for the second half of the year, including which goods to ship and by how much to raise prices.

Suppliers expect a large number of orders to be cancelled. This will force retailers to search for goods everywhere in the US and other markets to fill their shelves, even last year’s Christmas goods.