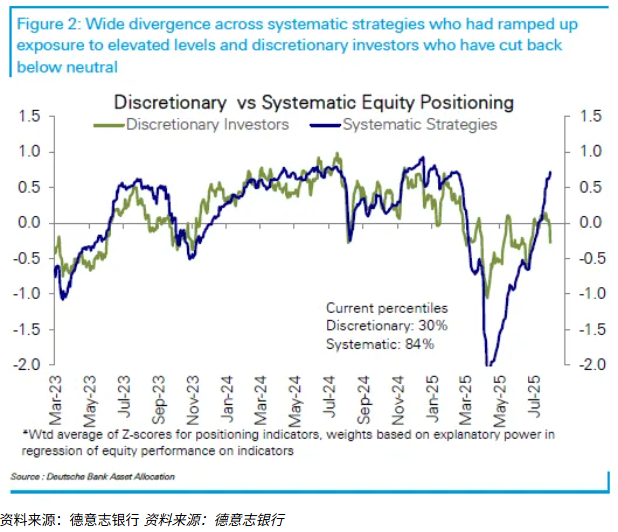

Parag Thatte, a strategist at Deutsche Bank, said that since the beginning of 2020 (before the worst of the pandemic), computer-guided traders have never been as bullish on stocks as human traders.

These two types of people form their views based on different clues, so it is not surprising that they have different opinions on the market. Computer-driven quick money quantitative analysts use systematic strategies based on momentum and volatility signals, while autonomous fund managers focus on economic and earnings trends to guide their investment actions.

However, such a degree of disagreement is rare, and historically, such differences do not last long, Tat said.

“Discretionary investors are waiting for some positive news, whether it’s a slowdown in economic growth or a spike in inflation due to tariffs in the second half of the year,” he said. “As the data comes in, if the market sells off due to concerns about economic growth, their concerns will either be proven correct; or the economy will remain resilient, in which case discretionary fund managers may start to increase their holdings of stocks based on optimism about the economy.”

Wall Street has made many confident predictions, but the reality is that no one knows what will happen with President Donald Trump’s trade agenda or the Federal Reserve’s interest rate policy.

As the S&P 500 index keeps hitting new highs, professional investors are no longer sitting on the sidelines. Data compiled by Deutsche Bank shows that as of the week ending August 1, due to the persistent uncertainties in global trade, corporate earnings and economic growth, professional investors have downgraded their stock holdings from “neutral” to “moderately underweight”.

Frank Moncam, the head of macro trading at Buffalo Rivermouth Commodities, said, “No one wants to buy stocks that are already at record highs, so some people are praying that any sell-off will be an excuse to buy.”

However, trend-following algorithmic funds are chasing this momentum. The significant reduction in positions during the spring paved the way for the rebound in recent months. As the S&P 500 index has rallied nearly 30% from its April low, these funds have been lured into a frenzy of buying. Data from Deutsche Bank shows that as of the week ending August 1, the long equity positions of systematic strategies reached their highest level since January 2020.

This divergence reflects a tug-of-war between technical and fundamental forces. The S&P 500 index, after experiencing its longest period of calm in two years in July, is currently fluctuating within a narrow range.

The Chicago Board Options Exchange Volatility Index (VIX) closed at 15.15 on Friday, approaching its lowest level since February. The index measures the implied volatility of benchmark U.S. stock index futures through out-of-the-money options. The VVIX index, which gauges the volatility of volatility, fell for the third time in four weeks.

Colton Loder, the executive director of alternative investment firm Cohalo, said: “The stretch of a rubber band is limited until it breaks. Therefore, when there is systemic crowding, as is the case now, the possibility of a mean reversion sell-off is higher.”

This kind of collective entry trading situation occurs regularly in computer-driven strategies. For instance, at the beginning of 2023, quantitative traders bought US stocks in large quantities after the S&P 500 index dropped by 19% in 2022, until volatility soared during the regional banking turmoil in March of the same year. At the end of 2019, after breakthroughs in the China-US trade negotiations, fast money traders pushed the stock market to new highs.

However, Sartor expects that this time the divergence between humans and machines will last for weeks rather than months. He said that if autonomous traders start selling due to a slowdown in economic growth or a weak trend in corporate earnings, thereby pushing up volatility, then computer-based strategies may also start to unwind.

In addition, Scott Rubner of Citadel Securities said that quick money investors might fully invest in US stocks by September, which could prompt them to sell stocks as they are vulnerable to the impact of a downward market.

Lord said that given the way systematic funds operate, the sell-off could start with commodity trading advisors (CTAs) unwinding extreme positions. He added that this would increase the risk of a sharp reversal in the stock market, although a sustained spike in volatility would require a significant sell-off to occur.

Goldman Sachs Group data shows that CTA has been a loyal buyer of stocks, holding $50 billion worth of long positions in US equities, at the 92nd percentile of historical exposure. However, Maxwell Grinacoff, head of equity derivatives research at UBS Group, said that the S&P 500 index needs to break through 6,100 points, or fall by about 4.5% from last Friday’s close, before CTA starts selling stocks.

So the question is, as quantitative positioning extends to the bullish side and due to extreme uncertainty, stock market pressure increases. Can any rebound from now on really last?

“The market is starting to feel like it’s reached its peak,” Grinakov said, adding that given CTA positions are close to their maximum long size, the upside for stocks “may be exhausted in the short term.” “This is a bit worrying, but it’s not yet a cause for alarm.”