President Donald Trump has launched an unprecedented and escalating attack on the Federal Reserve, which could backfire and lead to higher long-term borrowing costs in financial markets and the economy.

For weeks, he has been harshly criticizing Federal Reserve Chair Jerome Powell for not slashing interest rates significantly to stimulate the economy. In Trump’s view, Powell has also failed to reduce the government’s debt burden.

He has nominated the chair of his Council of Economic Advisers to the central bank’s board and is now trying to remove the bank’s president, Lisa Cook, setting the stage for a legal battle over the institution’s political independence.

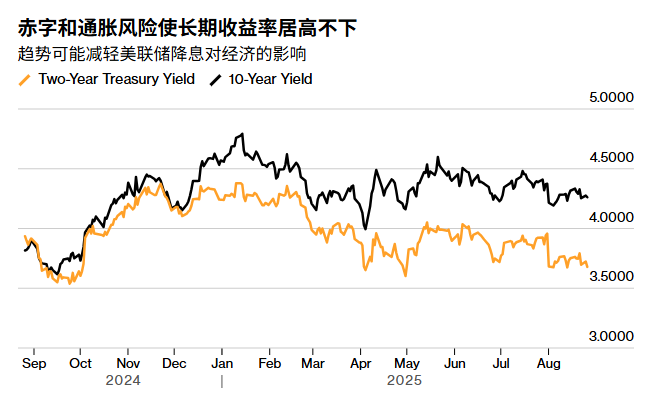

Although the Federal Reserve has considerable power over short-term interest rates, the 10-year U.S. Treasury yield (set in real time by traders around the world) largely determines how much Americans pay for trillions of dollars in mortgages, business loans and other debts.

Although Powell indicated that he is prepared to start easing monetary policy as early as next month, these interest rates remain high for other reasons: tariffs could exacerbate still-high inflation; the budget deficit will continue to inject new government bonds into the market; and Trump’s tax cuts could even provide a stimulus next year.

People are concerned that a Fed loyal to the president might cut interest rates too much and too quickly – thereby endangering the central bank’s credibility in fighting inflation – and that long-term interest rates could end up higher than they are now, thereby squeezing the economy and potentially disrupting other markets.

“Slower job growth in the US, combined with the White House’s provocation of the Federal Reserve – whether as an institution or individuals – is starting to pose real problems for US Treasury investors,” said David Roberts, head of fixed income at Nedgroup Investments. He expects long-term interest rates to rise even if short-term rates fall. “Inflation is far above the Fed’s target. Cheaper money now could trigger an economic boom, a weaker dollar and a sharp rise in inflation.”

Long-term interest rates are under pressure not only in the United States. In the UK, France and other countries, long-term interest rates are also supported by investors’ concerns over high government debt burdens and increasingly unpredictable political situations.

But the countercurrent of Trump’s return to the White House also brings its own challenges.

During last year’s presidential campaign, when investors began to bet on a Republican victory, the 10-year US Treasury yield rose sharply even as the Federal Reserve started to lower the benchmark overnight interest rate from its multi-decade high. This was because investors expected the Republicans’ tax cuts and deregulation agenda to inject momentum into the unexpectedly resilient economy at that time.

However, since Trump took office, the Federal Reserve has held its ground, as his unpredictable trade war has upended the economic outlook, spooked foreign investors and potentially pushed up consumer prices. In April this year, Trump’s tariff measures triggered one of the most severe bond sell-offs in decades, causing yields to soar. Trump then paused interest rate hikes, saying the market was “a little bit nervous, a little bit scared”.

Since then, he has reimposed import duties and his trade policy has continued to waver. Meanwhile, his tax cut bill is expected to increase the US deficit by more than 3 trillion dollars over the next decade, unless future presidents maintain his tariff policies and eventually generate sufficient revenue to offset the costs, which will further increase the US debt.

Michael Arone, chief investment strategist at State Street Global Advisors, said, “The United States must issue a large amount of debt to cover its deficit.”

He said that this excessive supply has intensified concerns over economic growth and inflation. “Therefore, I expect long-term interest rates to remain higher than market expectations and to be more volatile.”

Although Finance Minister Scott Bessent has said that the government’s cost-cutting and growth-promoting policies would eventually bring down the 10-year Treasury bond yield – which he has always regarded as a key benchmark for economic success – this has not yet happened. While short-term Treasury bond yields have fallen on expectations that the Federal Reserve will cut interest rates again, the 10-year Treasury bond yield rose as high as 4.31% on Tuesday before stabilizing at around 4.26%, roughly equivalent to the level when Trump was elected in November. The 30-year Treasury bond yield rose to 4.94%.