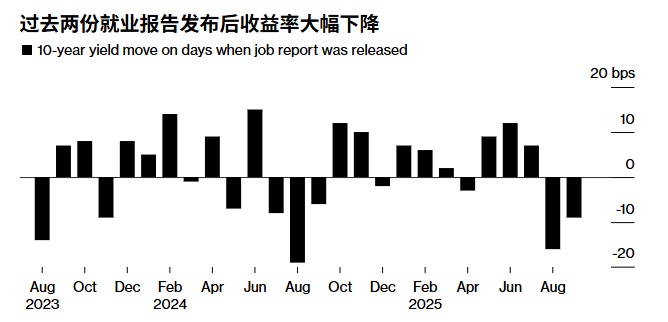

The biggest question facing bond investors in the coming days is whether the US monthly jobs report will shake their firm belief that the Federal Reserve will cut interest rates again as early as October.

Last week, traders reduced their bets on further easing by the Federal Reserve as officials were divided over monetary policy and some economic data came in stronger than expected. However, financial markets face a major challenge: the federal government may shut down on October 1, which could delay the release of key data, including the employment report due on Friday, one of the most closely watched economic reports.

Weakness in the job market prompted the Federal Reserve to cut interest rates for the first time this year this month. Traders expect a rate cut at the Fed’s meeting on October 28-29 with a probability of about 80%. But they may need more weak data to confirm the view that the labor market is cooling, solidify expectations for further easing by the Fed and keep US Treasuries on track for their best annual return since 2020.

James Athey, portfolio manager at Marlborough Investment Management, said the jobs report was “what’s needed to drive the economy to start rebounding from here – this is the key part of the story of a weak economy and dovish Fed policy.”

He said, “Even if we do see the data, it’s clear that the bar is still quite high to get a weak enough report to push yields down further.” He added that he is currently reducing his holdings of US Treasuries.

The 10-year Treasury yield climbed to 4.2% last week after falling to a five-month low of just under 4% on September 17. At that time, the Federal Reserve resumed its easing policy and cut interest rates by a quarter of a percentage point, although new Fed policymaker Stephen Miran opposed a half-percentage-point cut. The yield rebounded in part because data showed a decline in initial jobless claims and strong economic growth in the second quarter.

These reports prompted traders to slightly lower their expectations for easing, but they still strongly favor a 25 basis point rate cut next month and possibly in December. The market has priced in a total rate cut of about 1 percentage point over the next 12 months.

Traders have noted the weak government employment data in recent months, which led the Federal Reserve to make adjustments even though the inflation rate was above the 2% target. This move boosted the bond market. Bloomberg index data shows that U.S. Treasuries have risen 5.1% so far this year as of Thursday. This puts the market on track for its best performance since 2020.

A survey indicates that the government data to be released on October 3rd is expected to show that the number of non-farm jobs in the US increased by 50,000 in September, a rise from the average of less than 30,000 in the previous three months. Last week, Federal Reserve Chair Jerome Powell said that the recent pace of job growth “seems to be below the ‘break-even’ level needed to keep the unemployment rate stable.”

He restated that policymakers are confronted with the conflicting risks of a slowing labor market and rising inflation. There are also differences among officials on how to respond.

Chicago Fed President Austan Goolsbee expressed concerns last week about inflation driven by tariffs and rejected any calls for multiple “premature” rate cuts. Meanwhile, Fed President Michelle Bowman said that as the job market is weakening and inflation is already close enough to the central bank’s target, further rate cuts are necessary.

Market positions also show a similar divergence. In the case of treasury bond options, there have been buyers targeting a 10-year treasury bond yield of 4% or lower by the end of November. Meanwhile, a client survey by JPMorgan shows a sharp increase in short positions on treasury bonds.

Sarah Devereux, global head of fixed income at Vanguard Group, said: “We believe that the current level of the 10-year US Treasury yield is roughly reasonable, with risks balanced between the downside risk from the fragility of the labor market and the upside risk from an improving growth outlook.” She added that if the yield rises to the upper end of the recent range, the company’s active fund managers tend to buy bonds, especially those with maturities of five to ten years.

The risk of a government shutdown has also raised the importance of unaffected data, including the ADP private-sector employment report released on October 1. Although ADP is not always a reliable leading indicator of official data, the downward revisions of government data in recent months have confirmed the weak performance in the private-sector reports.

“ADP data will have a huge impact,” said Ed Al-Hussainy, a portfolio manager at Threadneedle Investment in Columbia. He said that strong employment data would “raise many questions about the interest rate path and the timing of rate cuts next year.”