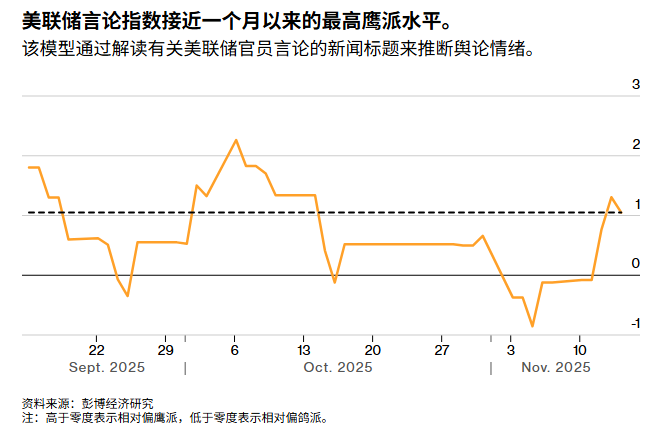

Some policy makers at the Federal Reserve have stepped up their warnings that the inflation process may slow down or stall, casting doubt on the prospect of another rate cut in December and exposing the deepening rift within the central bank.

Officials generally believe that the labor market has cooled down, but they are divided over whether the economic slowdown will intensify. Some are optimistic about price pressures, while others warn that the current interest rate level is almost unable to curb economic growth, and further rate cuts will endanger progress in inflation.

Such public disputes are rare. They reflect the current economic situation’s unpredictability and also the predicament faced by Federal Reserve Chair Jerome Powell, who is tasked with reaching a consensus on the direction of monetary policy.

William English, a professor at Yale School of Management and a former Fed department head, said, “They are facing a tough choice. I think people want to make their positions clear, so they are all speaking out and expressing their views. It is indeed a very challenging situation for the committee and Powell to reach a consensus.”

After advocating for rate cuts at the Fed’s last two meetings, Powell acknowledged that another cut is not a certainty. The views that prompted him to issue this warning have come to light recently, with some officials explicitly stating that they will not support a rate cut at the December 9-10 meeting.

Among them are several regional Federal Reserve Bank presidents, such as Jeff Schmitz of the Kansas City Fed and Susan Collins of the Boston Fed, who will all have a vote on interest rate decisions this year.

Those who oppose cutting interest rates have put forward two viewpoints. Firstly, they believe that the slowdown in job growth may reflect changes in immigration policies and technology rather than a severe deterioration in labor demand, which would lead to a sharp increase in the unemployment rate. Secondly, they point out that inflation risks not only include tariffs but also the resilience of overall consumer demand. They also note that inflation has been above the target level for several consecutive years, which has damaged the credibility of the Federal Reserve.

Schmid said on Friday: “I think further rate cuts will have little effect on healing any cracks in the labor market – these cracks are likely due to structural changes in technology and immigration policies. However, as our commitment to the 2% inflation target is increasingly questioned, rate cuts may have a more lasting impact on inflation.”

Collins also said this week that the rate cut in October was “prudent” and aimed at supporting employment, while warning that “providing additional monetary support to economic activity could slow down – or even prevent – inflation from returning to target.”

Josh Hirt, a senior US economist at Vanguard, said that concerns that households and businesses might question the Fed’s commitment to achieving its 2% inflation target are not unfounded. “You can never predict when that tipping point will come, but some things don’t matter until the last minute.”

But this does not mean that the dovish camp has conceded. Although they have become more low-key, they may still hold the majority among the voting members of the Federal Reserve’s policy-making committee.

Among them is Stephen Mnuchin, who was recently appointed as the central bank governor by President Donald Trump. Mnuchin believes that the current interest rate is significantly higher than the neutral rate that no longer restrains economic growth. He calls for a rapid and substantial rate cut to avoid potential damage to the labor market.

Milan’s view is rather isolated. However, some other governors, such as Christopher Waller and Michelle Bowman, remain more concerned about the labor market than inflation and thus support a rate cut. Although Powell was cautious towards investors after the last policy meeting, he seems generally at ease with the inflation issue.

Federal Reserve Vice Chair Philip Jefferson said on Monday that he believes the risks to the labor market are skewed to the downside, but he reiterated that as interest rates approach neutral, policymakers need to proceed with caution.

In a speech delivered at the Federal Reserve Bank of Kansas City on Monday, Jefferson said, “I think the risk balance in the economy has shifted in recent months, with downside risks to employment increasing and upside risks to inflation possibly having declined recently.”

As Powell’s term as chair ends in May, he may face more opposition from policymakers.

Powell acknowledged that officials had “very different views” on the December interest rate decision, but he generally regarded the dissents as a welcome part of the deliberative process.

“They are in a difficult position. This does indeed make Powell’s job more challenging,” said Inglis, a former Fed department head. “In such circumstances, even very wise and good policies may ultimately lead to bad outcomes because the situation is just too complex.”

Krishna Guha of Evercore ISI takes a more pessimistic view. In a recent report to clients, he noted that the current policy debate “feels like a dress rehearsal for the 2026 election, with officials under a Trump-appointed chair firmly opposing default spending cuts and insisting on data to back their views, ultimately leading to a deeply divided vote.”