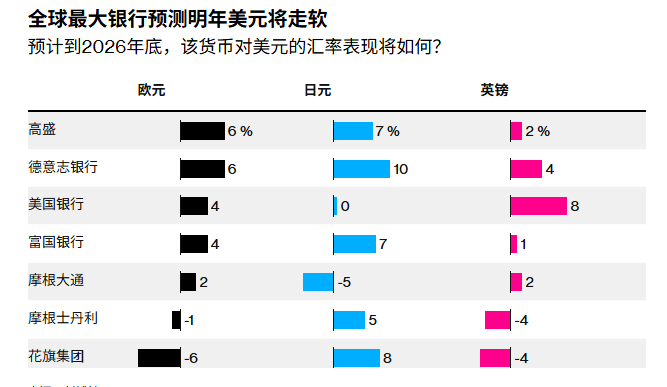

Deutsche Bank, Goldman Sachs and other Wall Street banks predict that the US dollar will continue to fall next year as the Federal Reserve keeps cutting interest rates.

In the first half of this year, the global market was thrown into chaos due to the trade war initiated by US President Donald Trump, causing the currency to plummet and record its biggest drop since the early 1970s. In the following six months, the currency stabilized.

But strategists expect that as the US central bank continues to ease monetary policy while other central banks maintain interest rates unchanged or edge towards hikes, the dollar will weaken again in 2026. This divergence will prompt investors to sell US Treasuries and shift funds to countries with higher yields.

Forecasters at more than six major investment banks generally believe that the US dollar will weaken against major currencies such as the Japanese yen, the euro and the British pound. The consensus forecast compiled by Bloomberg shows that the dollar index, a widely tracked index, will fall by about 3% by the end of 2026.

David Adams, head of G10 foreign exchange strategy at Morgan Stanley, said: “The market has enough room to digest a deeper rate-cutting cycle.” Morgan Stanley expects the US dollar to fall by 5% in the first half of this year. He added: “This means there is still a lot of room for the US dollar to weaken further.”

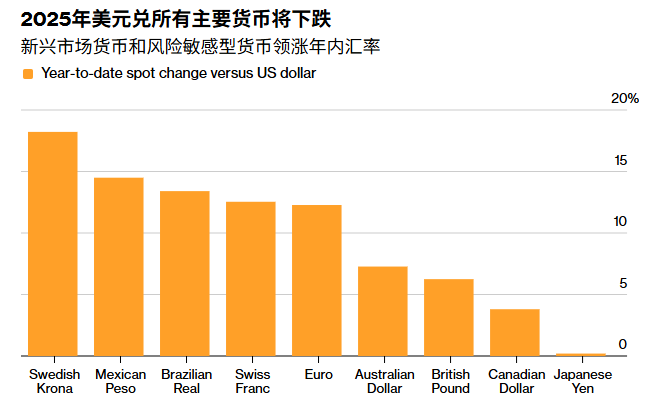

The decline of the US dollar is expected to be more moderate this year and not as significant as before. So far this year, the US dollar has fallen against all major currencies, causing the Bloomberg Dollar Spot Index to drop by nearly 8%, marking the biggest annual decline since 2017. This outlook hinges on the expectation of a persistently weak US job market – an expectation that remains uncertain given the surprising resilience of the post-pandemic economy.

Currency predictions have also been particularly challenging. At the end of last year, the US dollar soared as investors flocked to what was called the “Trump trade”, betting that his policies would boost economic growth. Strategists expected this rally to reverse by mid-2025, but were caught off guard by the extent of the dollar’s plunge in the first half of this year.

But strategists believe that the overall situation after the New Year indicates a weakening of the US dollar. Traders expect the Federal Reserve to cut interest rates twice next year, each time by 25 basis points. In addition, the Fed chairperson chosen by Trump may be pressured by the White House to cut rates further. Meanwhile, the European Central Bank is expected to keep interest rates unchanged, while the Bank of Japan may raise rates slightly.

“We believe the risks to the dollar are greater than those to the euro,” said Louis Kuijs, global head of macro research at JPMorgan in London, at a news conference on Tuesday.

A weaker dollar could have a ripple effect on the overall economy, pushing up import costs, boosting corporate profits overseas and promoting exports – all of which would likely be welcomed by the Trump administration, which has long complained about the US trade deficit. Moreover, as investors shift funds to emerging markets to take advantage of higher interest rates, a weaker dollar could also extend the rally in emerging markets.

Goldman Sachs’ analyst team, including Kamakshya Trivedi, also pointed out this month that after other G10 currencies such as the Canadian dollar and the Australian dollar released stronger-than-expected economic data, the market began to factor in a more optimistic economic outlook into the exchange rates of these currencies. They noted that the US dollar “tends to depreciate when the economic situation in the rest of the world is good.”

Those contrarian investors who expect the US dollar to strengthen against other major currencies are mainly targeting the robust US economy. Analysts from Citigroup and Standard Chartered Bank say that the booming development of artificial intelligence will drive US economic growth, attract investment inflows and thus push up the value of the US dollar.

“We believe the dollar cycle has strong recovery potential in 2026,” wrote the Citigroup team led by Daniel Tobon in its annual outlook.

On Wednesday, Fed policymakers raised their growth forecast for 2026, highlighting the possibility of stronger-than-expected economic growth. However, they still cut interest rates by 0.25 percentage points and continue to plan one more rate cut next year. Powell also dispelled concerns that the Fed might shift to raising rates, saying the current debate is over whether the Fed should continue cutting rates given the weak job market and inflation still above target, or wait for the right moment.

George Saravelos, global head of foreign exchange research at Deutsche Bank in London, and his colleague Tim Baker in New York, pointed out in their annual outlook report sent to clients at the end of last month that the US dollar has benefited from the “astonishing resilience” of the US economy and the rise of the US stock market. However, they also said that the dollar is overvalued and predicted that it will weaken against major currencies next year as economic growth and stock returns in other regions rebound.

They wrote: “If these predictions come true, it will confirm that the unusually long bull market cycle of the US dollar in this century has come to an end.”