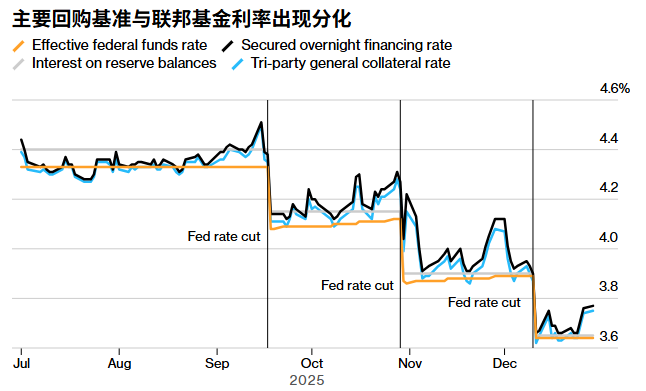

A survey by the Federal Reserve shows that respondents expect the total amount of reserve management purchases by the central bank as one of the measures to ease pressure in the money market to exceed 200 billion US dollars in the next 12 months.

Fed policymakers decided at their December 9-10 meeting to start buying Treasury securities because they believed that the reserves in the financial system had fallen to a level that indicated a rise in short-term financing costs. Although bank reserve levels fluctuate over time, cash demand tends to increase at the end of the month and quarter as tax payments and other settlement amounts come due.

The minutes of the Federal Open Market Committee’s December 9-10 meeting, released on Tuesday, stated: “Although respondents’ estimates of the expected purchase size varied widely, on average, respondents expected net purchases of approximately $220 billion in the first 12 months of the purchase.”

The Federal Reserve said it would purchase about $40 billion of Treasury bills each month and then gradually reduce the purchase scale. So far this month, the Federal Reserve has purchased about $38 billion of Treasury bills and will conduct two more operations in January.

Fed policymakers stressed that these purchases are merely tools for managing reserves and are distinct from the central bank’s broader monetary policy or efforts to stimulate the economy.

The minutes of the meeting indicated that some participants noted that the pace of increase in money market rates relative to the rates managed by the Federal Reserve was faster than during the balance sheet reduction period of 2017-2019, and thus this decision was made.

Early this month, the Federal Reserve halted its reduction in the size of its Treasury holdings (i.e., quantitative tightening) as signs of stress in the $12.6 trillion repo market became increasingly evident. Since the summer, the issuance of Treasury bonds has continued to grow, and combined with the quantitative tightening policy, this has led to a drain of funds from the money market, exhausted the Fed’s main liquidity tools, and pushed up short-term interest rates.

Worryingly, insufficient liquidity could disrupt the important operating mechanisms of the financial market, weaken the Federal Reserve’s ability to control interest rate policies, and in extreme cases, force fluctuations in market positions, which in turn could affect the broader Treasury market, which serves as the benchmark for global borrowing costs.

The minutes of the December meeting also recorded the discussions among Fed officials on how best to maintain bank reserves at an appropriate level. Some participants emphasized that, given the possibility of changes in demand, it would be more attractive to focus on the relationship between money market interest rates and the interest on reserves rather than on a specific level of reserves.

According to data released by the Federal Reserve Bank of New York on Tuesday, the key benchmark rate closely related to the overnight funding market – the Secured Overnight Financing Rate (SOFR) – was locked at 3.77% on December 29. This was 12 basis points higher than the interest rate on Federal Reserve reserve balances.

The minutes of the meeting stated: “Some participants indicated that if the definition of ‘adequate reserves’ led to a supply of reserves in excess of what was needed to implement the Committee’s framework, it could result in excessive risk-taking by leveraged investors.”

Some Fed officials also suggested that the standing repo facility, which serves as a liquidity backstop, could “play a more active role” in interest rate control and, on average, could reduce the size of the balance sheet. However, other officials indicated that they preferred to rely more on reserve management purchases.