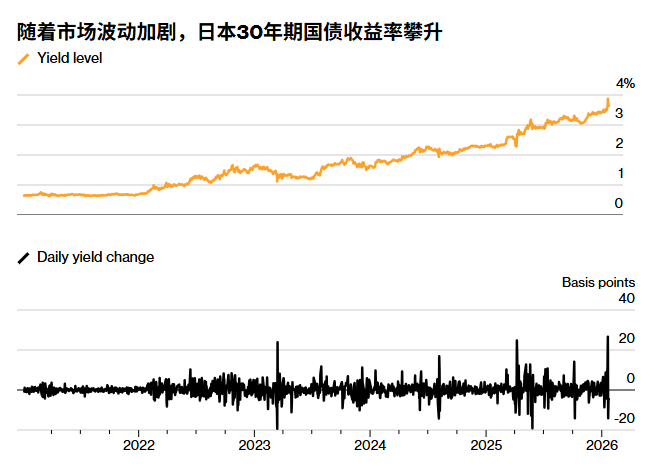

After several days of sharp falls in Japanese government bonds, the global financial markets were shaken, and traders were still stunned by the speed and extent of the decline. Pramol Dhawan, a fund manager at Pacific Investment Management Co., marveled that yields had jumped by 0.25 percentage points in a single trading day, which he found “incredible”.

In the past, it took weeks or even months for yields in Japan’s government bond market to fluctuate slowly to such a large extent. For most of the 21st century, the Japanese government bond market was exceptionally stable, and interest rates remained at extremely low levels. As a result, Tokyo was regarded by investors around the world as a source of cheap financing and stability during global turmoil.

Last week’s sell-off, accompanied by wild swings in the yen, made it clear that the good times are over. Japan’s long-dormant inflation has flared up, and Prime Minister Suga Yoshihide’s fiscal stimulus plan will further exacerbate the already worrying level of government debt. As a result, investors have been frantically selling bonds, pushing yields to unprecedented levels – the yield on the longest-dated Japanese government bond has exceeded 4%. This has put upward pressure on interest rates from the United States to the United Kingdom and Germany.

With Japan’s snap election on February 8th, traders are bracing for more volatile market swings. Both Kishida and her rivals have made loose budget policies the cornerstone of their election platforms. In the long run, what global markets are more concerned about is that the new normal of rising Japanese government bond yields will prompt domestic investors to repatriate more funds. Currently, Japan has about $5 trillion in capital invested overseas, not including the yen borrowed by foreign funds for global financial asset investment.

“This is a new era,” said Masayuki Koguchi, executive chief fund manager at Mitsubishi UFJ Asset Management, one of Japan’s largest asset management companies. “I think Japanese yields haven’t fallen enough yet. This is just the beginning – there could be a much bigger shock in the future.”

Since the Bank of Japan ended its negative interest rate experiment in March 2024, the sell-off in Japan’s $7.3 trillion government bond market has intensified and become more frequent, with nine declines exceeding two standard deviations of the average for the same period.

Even by these standards, Tuesday’s sell-off was particularly striking. Kishida Fumio’s announcement of an early general election, aimed at consolidating his power and ensuring support for his high-spending and tax-cutting policies, sent ultra-long-term bonds into a tailspin, wiping out $41 billion from Japan’s yield curve. The yield on 40-year government bonds soared above 4%, a record high, while the yield on 30-year bonds rose by more than 0.25 percentage points – eight times the average daily trading fluctuation over the past five years.

This shockwave swept across the globe, causing a sharp drop in US Treasury bonds and unexpectedly becoming the focus of attention for the financial magnates gathered in Davos, Switzerland, to discuss the historic geopolitical turmoil this year. By the end of the day, US Treasury Secretary Scott Bessent called Japanese Finance Minister Mayumi Otsubo to inform her that the US market had also been affected by the sell-off. An analysis by Goldman Sachs indicated that every 10 basis points of the “Japan-specific shock” would exert an upward pressure of approximately 2 to 3 basis points on yields in the US and other regions.

The yen’s exchange rate rebounded rapidly after speculation about Japanese government intervention began to spread in Tokyo’s trading halls. Then it was reported that the Federal Reserve Bank of New York had contacted several financial institutions to inquire about the yen’s exchange rate – a strong signal for anyone shorting the yen that authorities in Japan and the United States might be preparing to intervene. Some people believe this once again indicates that the Trump administration is concerned that the turmoil in Japan could pose a threat to the US market.

Anthony Doyle, chief investment strategist at Pinnacle Investment Management, said: “If the yen depreciates significantly, Japan will have to defend it, and the quickest way is to sell foreign exchange reserves, including US Treasuries. That’s why Japan’s problem could turn into a rise in US Treasury yields at the most inopportune time.”

It is still unclear how high the yield needs to be to prompt a large-scale repatriation of Japanese investors’ funds. But many large institutions are more optimistic about their domestic market.

Sumitomo Mitsui Financial Group, Japan’s second-largest bank, said last week that it would significantly adjust its government bond investment portfolio and reduce its allocation to overseas markets. Yukihiro Nagata, the group’s global markets chief, said in an interview: “I used to love investing in overseas bonds, but not anymore. Now I only invest in Japanese government bonds.”

Last year, the yield on 30-year Japanese government bonds was higher than that of Germany and China. A recent trading report from Goldman Sachs Group Inc. pointed out that its yield would eventually rise to the same level as that of the 30-year US Treasury bonds.

The closely watched 10-year government bond yield is also on the rise – this benchmark yield is crucial to borrowing costs across the entire financial market and was once the cornerstone of the Bank of Japan’s yield curve control mechanism. Koguchi of Mitsubishi UFJ Bank said that if there is no policy shift in Japan, the 10-year government bond yield could rise by at least 1.25 percentage points to 3.5%.