Banks are issuing a record amount of risk transfer bonds at a rapid pace, using the tool to hedge against broader loan risks, including leveraged buyouts and financing.

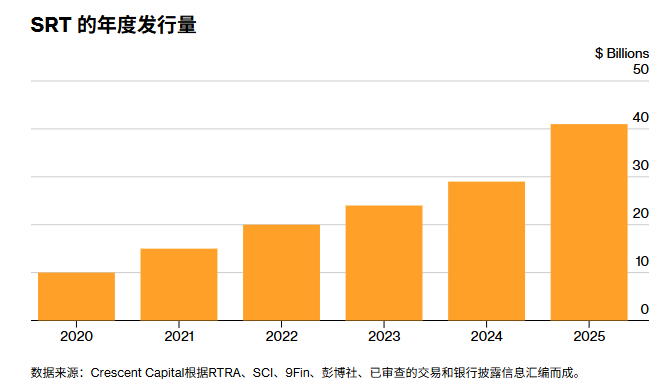

According to data from credit investment firm Crescent Capital, lenders mainly from Europe and North America issued $41 billion in Special Resolution Tool (SRT) bonds in 2025, up from $29 billion the previous year. Juan Granado, head of bank capital solutions at Crescent Capital, told Bloomberg that this indicates SRT issuance is on track to grow by more than 20% this year, and there are no signs that the Middle East conflict will delay transactions.

The issuance of securities risk transfer (SRT) bonds, a way for banks to insure against loan defaults, has hit record highs for five consecutive years. Several lenders, including Deutsche Bank, ING and NatWest, have recently said they will increase their issuance of SRTs, indicating that the asset class will continue to grow rapidly.

In response to an email inquiry, Granat said, “While some of the most active banks are consolidating their bond issuance operations, we are seeing many new entrants expanding the use of bonds. We have witnessed growth in all major markets (Europe, the United States, and Canada), and we expect this growth momentum to continue.”

According to Crescent Capital’s report, large enterprise loans remain the most commonly used collateral type for SRT, accounting for nearly half of the total. Lenders are increasingly referring to other types of debt, with high-yield loans and leveraged loans currently making up 11% of SRT issuance. The report also found that fund financing transactions account for another 6%.

This is reflected in the recent completion by BNP Paribas of a securities-based lending transaction (SRT) related to credit from a US business development company (BDC). The French bank is also actively seeking investors for the planned issuance of two additional securities-based lending transactions, one involving loans to wealthy clients and the other related to leveraged buyout financing.

Last year, Morgan Stanley discussed a transaction in the United States related to what is called a subscription capacity arrangement, which is typically offered to private equity and other private market funds.

Banks typically obtain guarantees equivalent to 5% to 15% of the loan amount. This enables them to enhance their solvency ratios and reduces their reliance on less favorable financing methods for shareholders, such as issuing new shares. Additionally, it increases their flexibility in making new loans, conducting acquisitions, or distributing dividends to shareholders.

New Moon Capital said that the total size of the loan portfolio protected by the Special Risk Transfer mechanism (SRT) last year rose to as high as 500 billion US dollars, compared with 350 billion US dollars in the previous year.

The investment company stated that European and British lenders account for over 70% of SRT issuance, followed by the United States and Canada, which hold 21% and 4% respectively. It is expected that this dominance will continue, although the use of SRT is expanding to other regions.

“We are seeing banks in Asia, the Middle East and Africa now also considering bond issuance,” said Granat, who was once a banker at institutions such as Credit Suisse and Nomura Holdings.

In a report in February, Fitch Ratings said that banks interested in entering the Saudi Arabian market include SEB AB of Sweden and DBS Group Holdings Ltd. of Singapore. Lenders in Saudi Arabia may incorporate SRT (securitization transactions) as part of their strategy to cope with the expanded loan scale for financing the country’s major infrastructure projects.

Although credit investors are struggling to cope with the impact of the Middle East war on energy prices and supply chains, the SRT market has shown strong resilience to major geopolitical events, including Russia’s invasion of Ukraine. Granah said that the deals currently under negotiation are still ongoing.

Granah said, “It’s still too early to judge how the recent events will affect the market. We haven’t found any disruptions to current pricing or ongoing transactions. The period of 2022-2023 was a good test of the potential impact of major geopolitical events. Not only did the market continue to operate normally, but it also kept growing.”