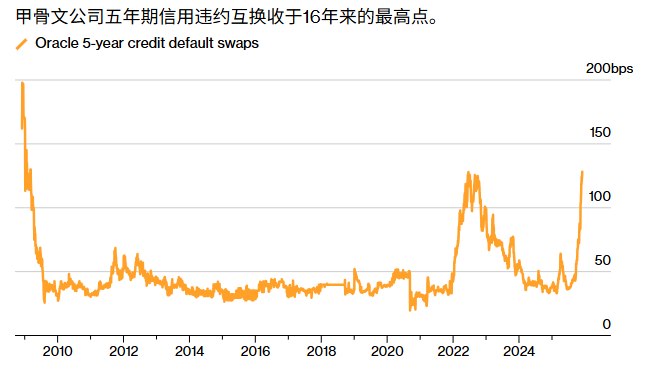

After tech giants’ large-scale bond issuance intensified concerns that a bubble was forming in the artificial intelligence industry, Oracle’s credit risk indicator for debt closed at its highest level since the financial crisis.

According to ICE Data Services, the cost of protection against Oracle’s debt default, based on credit derivatives prices at the New York close, reached its highest level since March 2009 on Tuesday, at around 1.28 percentage points per year. The price rose by nearly 0.03 percentage points from the previous day and has more than tripled from the June low of 0.36 percentage points.

In recent months, Oracle has actually sold tens of billions of dollars in bonds through direct bond issuance and indirect support for its investment projects. These bond issuances, coupled with Oracle’s credit rating being lower than that of other cloud computing giants, have made the company’s credit default swaps a key way for investors to hedge against the risk of an AI crash.

The rise in the cost of default protection reflects investors’ concerns about the gap between the huge investment in the artificial intelligence sector and when productivity gains and corporate profits will materialize. Hans Mikkelsen of TD Securities warns that this boom is similar to previous market manias that pushed asset prices to extremes before they fell back to normal levels.

The strategist said in an interview, “We have experienced similar cycles before. I can’t prove that this time is exactly the same, but it looks very similar to what we saw before, such as during the dot-com bubble.”

A representative of Oracle Corporation declined to comment.

Morgan Stanley issued a warning in late November that Oracle’s growing debt could push its credit default swap rate closer to 2 percentage points, slightly above the historical high in 2008. The rate reached 1.30 percentage points on Tuesday, the highest since the New York close in March 2009.

Oracle, headquartered in Austin, is the lowest-rated among leading hyperscale data center operators. The company issued $18 billion in US investment-grade corporate bonds in September, and its data centers are closely related to the largest artificial intelligence infrastructure deal in the market. Oracle’s AI ambitions are closely tied to OpenAI, and the database company expects to generate hundreds of billions of dollars in revenue from OpenAI in the coming years.

According to data compiled by Bloomberg, as of the end of August, Oracle Corporation had liabilities of approximately $105 billion, including lease debt. About $95 billion of this debt is currently issued in the form of U.S. Treasuries and is included in the Bloomberg U.S. Corporate Bond Index. The company is the largest issuer in the index outside of the banking sector.

Recently, investors have been snapping up credit default swap (CDS) contracts on the debt of this BBB-rated company. Jigar Patel, a credit strategist at Barclays, analyzed data from a trading database and found that the trading volume of Oracle’s CDS soared to about $5 billion in the seven weeks ending November 14, compared with just over $200 million in the same period last year.

At the same time, the spending boom for building artificial intelligence infrastructure and expanding power capacity to meet its demands is expected to continue until next year. Mikelson of TD Bank predicts that the issuance of investment-grade bonds in the United States will reach a record high of 2.1 trillion US dollars in 2026. Bloomberg News data shows that the issuance this year has already exceeded 1.57 trillion US dollars.

Strategists say that the ability of corporate bondholders to profit from the AI boom is limited. If companies continue to pour huge sums into AI investment, fund managers may find the credit quality of their bond investments deteriorating.

Citigroup strategists wrote: “Investors are increasingly concerned about how much supply there may be in the future. This indecision has had a significant impact on the industry’s spreads.”