Copper prices rose to a record high as the United States and China are on the verge of reaching a comprehensive deal to ease trade tensions and alleviate a major risk to global economic growth.

The global benchmark price on the London Metal Exchange rose by 0.9% to $11,065.50 per ton, just $50 short of its highest level since the first half of 2024.

U.S. Treasury Secretary Scott Bessent said that Trump’s plan to impose a 100% tariff has been “canceled”, and Beijing will suspend its plan to expand rare earth export controls for one year.

Last May, copper prices hit a record high of $11,104.5 per ton. At the beginning of this month, they broke through the $11,000 mark again. Since then, copper prices have been fluctuating due to the tough stances taken by China and the United States ahead of their trade negotiations. This year’s strong performance of copper prices – with LME copper prices rising by about a quarter – is largely attributed to a series of mine accidents in major copper-producing countries.

Freeport-McMoRan Inc. cut its copper sales forecast in September following a fatal accident at its giant Grasberg mine in Indonesia. Ivanhoe Mines Ltd.’s Kamoa-Kakula mine in the Democratic Republic of Congo also suffered a major production setback.

The dollar’s decline this year has further pushed up metal prices, making dollar-denominated commodities more attractive. As investors bet on further rate cuts by the Federal Reserve, a gauge of the dollar’s strength has fallen by more than 7% since January.

Copper prices also reflect the widespread optimism about the energy transition. BHP Group, the world’s largest mining company, predicts that global copper demand will increase by about 70% by 2050 and regards copper as its main growth opportunity.

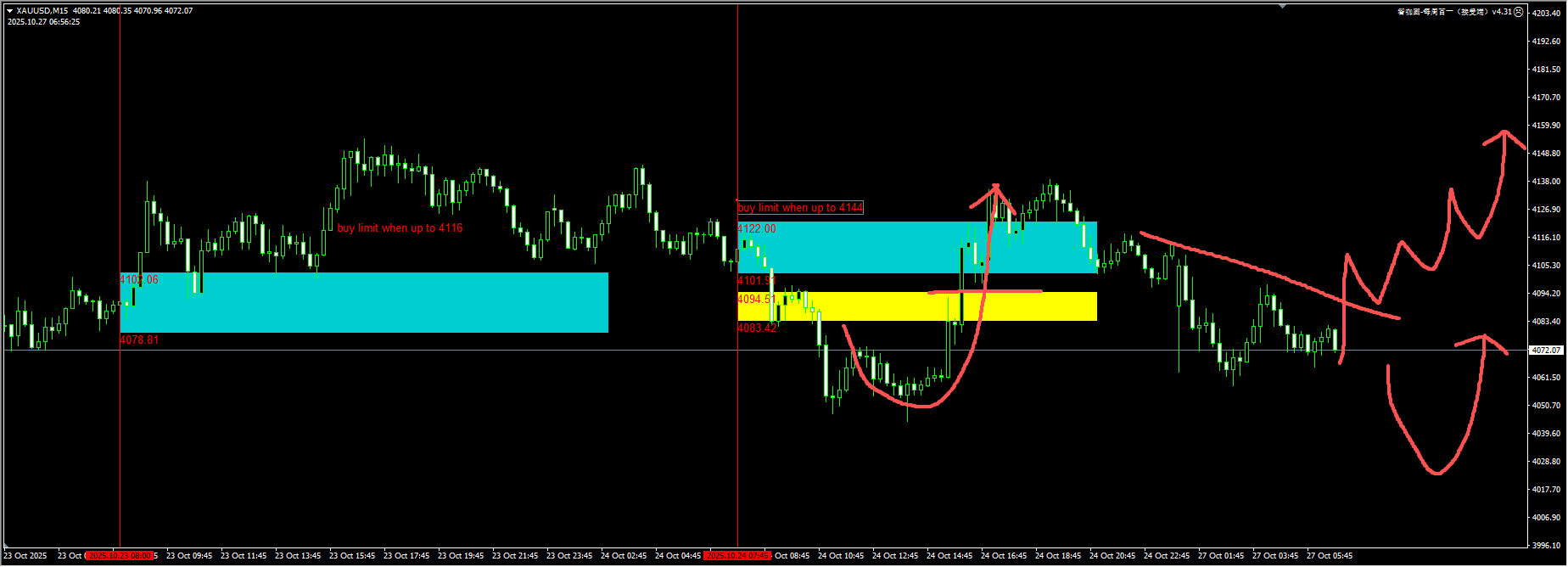

Technical analysis:

The WeChat functions may be restricted from time to time. If you want to experience the plugin, please leave your contact information when adding a friend so that we can add you back easily!!!

Gold: The easing of Sino-US trade tensions has weakened the partial support for gold from safe-haven demand. However, the overall situation has not changed significantly. This week’s focus will be on the outcome of the Federal Reserve meeting and whether it will further hint at halting the reduction of its balance sheet. Our observation of gold remains focused on capturing bullish signals. For detailed positions, please consult the plugin.

(Gold 15-minute chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the chart, please contact V: Hana-fgfg and leave your contact information for us to get back to you.

The Nasdaq continued to hit new highs as tensions eased around TACO trading and potential progress in Sino-US trade negotiations. We remain vigilant for rebound signals following the low liquidity sweep and caution against chasing the rally. For detailed positions, please consult the plugin.

(NASDAQ 15-minute chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the chart, please contact V: Hana-fgfg and leave your contact information in the message for us to get back to you.

Crude oil: After a continuous rebound and recovery for about a week, the oil price trend has entered a sideways consolidation pattern. Operationally, it is necessary to wait for a confirmed breakthrough signal before considering any action. Meanwhile, pay attention to the rebound signal after the low-sweep liquidity. For detailed positions, please consult the plugin.

(Crude Oil 15-Minute Chart)

The plugin is updated from 12:00 to 13:00 every trading day. If you want to experience the same plugin as shown in the picture, please contact V: Hana-fgfg and leave your contact information in the message for us to get back to you.