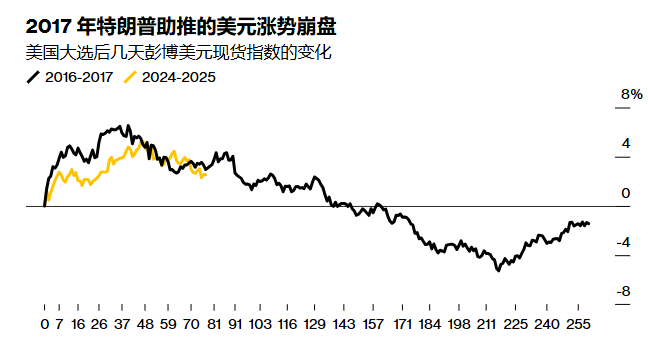

Morgan Stanley said that the factors that led to the depreciation of the US dollar in the early days of Donald Trump’s first term will again threaten the dollar’s exchange rate in 2025.

Morgan Stanley strategists Andrew Watrous, Ariana Salvatore and Arunima Sinha believe that a month after the start of Trump’s second term, many catalysts are once again clouding the dollar and could lead it to follow a similar trajectory this year as it did in 2017.

“Why did the US dollar fall in 2017? Trade policy, global growth and European politics were all among the reasons,” they wrote in a report on Monday. “We believe the reasons for the dollar’s decline this year are the same as those in 2017.”

In recent months, the dollar’s performance has taken investors by surprise. The Bloomberg Dollar Spot Index rose by more than 4% from election day to the end of 2024, as investors bet that the new Trump administration’s high tariffs would reignite inflation and push up US bond yields.

This year, the upward trend of the US dollar has reversed. After experiencing its worst three-week performance since September, the US dollar index has dropped by 2%.

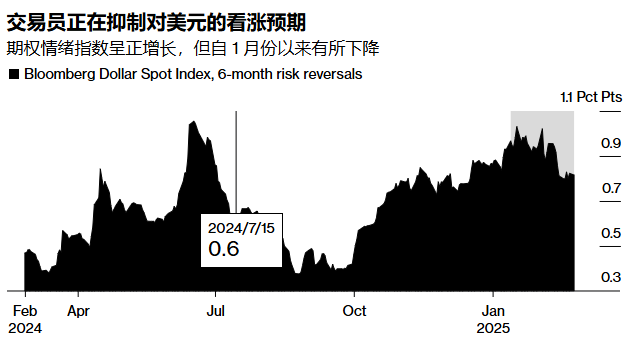

The bank said that the tariff policy was not as strict as many investors had expected, which was one of the reasons for the weakness of the US dollar. Trump said last week that he might impose about 25% tariffs on imports of automobiles, semiconductors and medicines, and the announcement would be made as early as April 2. Trump had previously threatened to impose tariffs on Canada, Mexico and Colombia, but later withdrew the threat, which increased the possibility that his latest proposal might also be a negotiating tool.

However, the 10% tariff on Chinese imports and the 25% tariffs on steel and aluminum imports will take effect on March 12.

However, about 30% to 40% of the investors surveyed by Morgan Stanley do not believe that the United States will impose comprehensive reciprocal tariffs, and they think that the series of April deadlines are merely aimed at forcing the other side to make “geopolitical concessions”.

In the coming months, the political situation in Europe is another potential pressure on the US dollar. Strategists at Morgan Stanley say one focus is the aftermath of the German election. The possibility of a coalition between the Christian Democratic Union-led bloc and the Social Democratic Party could boost the euro.

Analysts at Bank of America also keep a close eye on the euro-dollar exchange rate. In their report on February 21, they stated that the euro-dollar exchange rate is the “foreign exchange center of uncertainty in U.S. foreign policy.”

They predict that the euro will reach 1.10 against the US dollar by the end of this year and say that a lot of positive news has already been reflected in the exchange rate of the US dollar against the euro. The euro recently traded at around 1.0475 against the US dollar.

Goldman Sachs strategists, including Kamakshya Trivedi, also believe that the outlook for the US dollar is similar to that of 2017. However, the bank said that if the US starts to take more concrete measures to support its tariff negotiations, the dollar could rebound – as it did in 2018.

The parallels with today are obvious, and the risk of a repeat is rising, Trivedi and his team wrote in a report on February 21, comparing it to 2017. However, there are also clear similarities between today and early 2018 – when the US announced new steel and aluminum tariffs, engaged in tense trade negotiations with Canada and Mexico, and was preparing to raise tariffs on China.