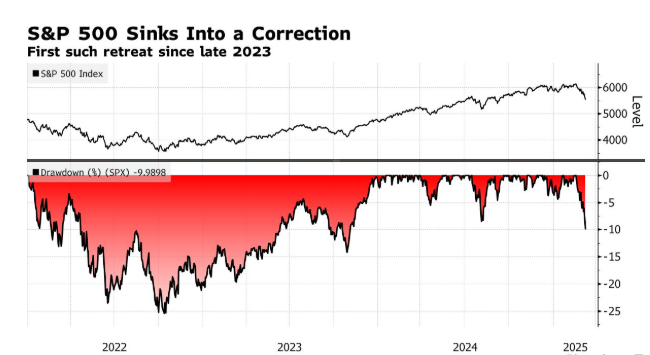

The latest round of trade policy news triggered another volatile trading day on Wall Street. The S&P 500 index has fallen for three consecutive weeks, with the decline once reaching 10%, but then rebounded to narrow the loss.

The index closed down 0.5%, after having dropped as much as 1.5% earlier. This suggests that the index is on track to meet the widely recognized definition of a correction, which would be the first since the end of 2023. Currently, the index is trading at 5,572 points, compared with a closing high of 6,144.15 points set last month. Technology giants Apple, Nvidia and Alphabet were the biggest contributors to the index’s decline on the day. The tech-heavy Nasdaq 100 index entered a correction on March 7, falling 0.2%.

As in the past three weeks, the rapid development of the Trump administration’s trade policy led to significant fluctuations in the stock market on Tuesday. Shortly after 10 a.m., President Trump threatened to raise tariffs on Canada, triggering the biggest drop of the day. When the index fell 10% from its all-time high, bargain hunters stepped in. News that Canada would delay imposing some retaliatory tariffs and that Ukraine would accept the U.S. plan for a ceasefire with Russia in exchange for aid helped fuel the rebound. However, the market closed lower, with all tariffs on aluminum and steel imports set to take effect at midnight.

Even after the rebound, the CBOE Volatility Index remained above 27, and market sentiment remained fragile.

Adam Sarhan, the founder of 50 Park Investments, said: “We are in a situation where the tide is turning and fear is taking over. This is largely due to the unwinding of the ‘Trump trade’, but it’s also related to concerns about future growth and the ‘R’ word – recession.”

In recent weeks, stock market sentiment has deteriorated rapidly as economists have downgraded their growth forecasts on the possibility of a fierce trade war. On March 9, US President Donald Trump told Fox News that the US economy was facing a “transition period” and refused to rule out the possibility of a recession, further intensifying these concerns.

Dennis DeBusschere of 22V Research wrote in a report to clients: “For the US economy, a reasonable base case is that the growth trend over the next year or so will be between 1.5% and 2% based on the implementation of tariffs, lower than the roughly 2.5% of the past few years.”

Meanwhile, as investors have grown skeptical about the near-term prospects of artificial intelligence and more broadly pulled back from riskier growth assets, the large-cap technology stocks that have driven the S&P 500 up by more than 50% over the past two years have fallen into a sell-off.

Meanwhile, sell-side strategists are warning of rising stock market volatility. Morgan Stanley predicts that the S&P 500 will fall by 5% to 5,500 points in the first half of the year due to the impact of tariffs and reduced fiscal spending on corporate earnings. JPMorgan Chase and RBC Capital Markets have also lowered their bullish expectations for 2025.

The trend of investors avoiding risks has been reflected in the sector performance of the S&P 500 index this year. Non-essential consumer goods and information technology stocks usually perform strongly when the economy is healthy, but in 2025, they will be the sectors with the largest declines, while defensive sectors such as healthcare, real estate and essential consumer goods will lead the decline.

Tariff noise has also widened the benchmark index’s lagging performance compared with its global peers. The US stock index has fallen behind those of Europe, China, Mexico and Canada.

“Bearishness is currently dominant. Every time the market attempts to rebound, we witness another sharp decline,” said Salhan. “If this persists, in a few days, we will see the market environment completely shift from bullish to bearish.”