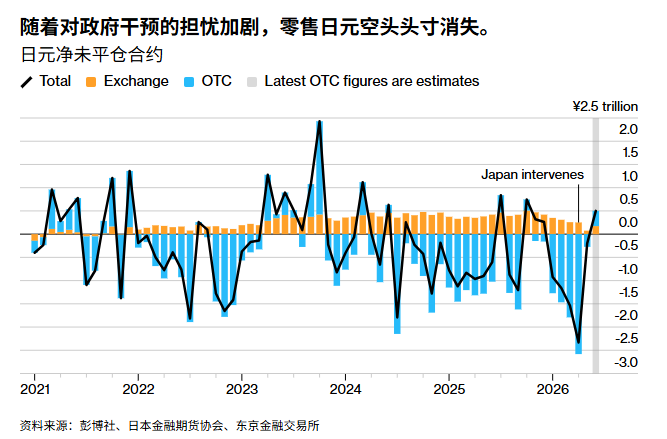

Japan’s large retail forex traders heeded government warnings and stopped betting on the yen’s depreciation, diverging from professional investors who continued to bet on further yen weakness.

According to Bloomberg’s analysis of data from the Japan Financial Futures Association and the Tokyo Financial Exchange, individual investors’ average yen position has turned into a net long position of approximately 500 billion yen (3.1 billion U.S. dollars). In contrast, yen short positions stood at 2.33 trillion yen at the end of April, the highest level since late 2020.

On Monday, the yen fell to 161.93 against the dollar, breaking below the level at which Japan’s Ministry of Finance intervened in late April to support the currency, raising the risk of further Japanese intervention. Despite the Bank of Japan’s rate hikes, the yen continues to face sustained pressure. Investors believe the central bank has acted too slowly to effectively narrow the interest rate gap between Japan and other major economies.

“Retail investors may be building reverse short-dollar, short-yen positions, anticipating Japanese intervention,” said Marito Ueda, managing director at SBI FX Trade in Tokyo.

In contrast, according to the latest data from the U.S. Commodity Futures Trading Commission for the week ending June 16, leveraged funds and asset management companies collectively held the largest net short position in the yen since July 9, 2024, approaching the record short position set just a week earlier.

This move by professional investors appears to ignore repeated warnings from Japanese Finance Minister Mayumi Kajiyama, who has stated that authorities are prepared to take “bold actions” to curb excessive speculation in the foreign exchange market. According to Japan’s public broadcaster NHK, Kajiyama and senior Japanese monetary policy official Atsushi Muramura held an online meeting on Monday with U.S. Treasury Secretary Scott Bessent.

Market volatility tends to be more intense when the yen rises than when it falls. This year, concerns over market intervention have suppressed the yen’s depreciation, widening the gap between the magnitude of yen appreciation and depreciation.

The risk of sharply rising volatility during yen appreciation is unfavorable for yen-funded carry trades, a strategy in which investors sell yen to buy higher-yielding assets and profit from the interest rate differential.

Ray Atre, head of foreign exchange strategy at National Australia Bank Limited, said the U.S. dollar against the Japanese yen is “currently in a dilemma: on one hand, there’s the risk of intervention; on the other, persistent arbitrage opportunities from shorting the yen.” He was referring to Japan’s potential intervention and noted that “the USD/JPY exchange rate could again fluctuate within the 162–163 range.”

FFAJ data shows that off-exchange retail trading volume dropped to its lowest level since February 2024 last month, indicating cautious sentiment among individual traders.

“Even though market expectations of continued yen weakness are deeply entrenched, local retail investors may still be reluctant to touch the yen,” said Ayako Sera, senior market strategist at Sumitomo Mitsui Trust Bank in Tokyo, as intervention could trigger increased yen volatility.